How Disability Insurance Works

How disability insurance protects your income - covering own-occ vs. any-occ, payout %, employer vs. individual, and family needs.

Happy National Boss’s Day!

Celebrate unforgettable bosses - like mine Tony Russo, Gary Austin, Thushan Wijesinghe, and Orna Samuelly - who led with calm, care, clarity, humor, and kindness.

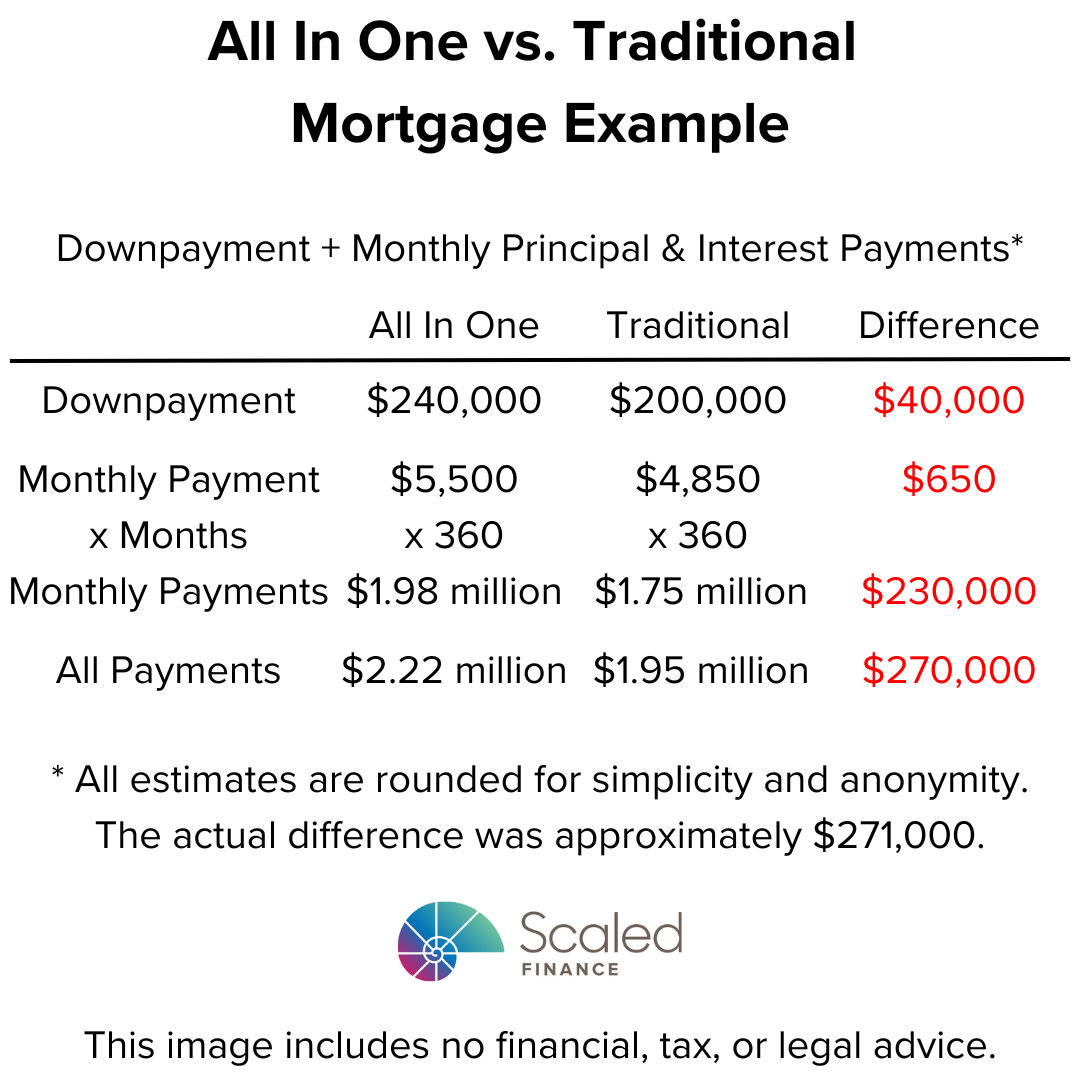

Could an All In One Mortgage Cost an Extra $270,000?

How an ‘all in one’ mortgage could cost $270,000 more over time - and why a traditional mortgage might be smarter.

Charge Market Rent!

Why charging market rent can boost your cash flow, lift property value, and avoid income loss over years.

Schedule Your PTO ASAP

Schedule your Paid Time Off (PTO) as soon as possible!

Lodging gets booked

Flight prices rise

Schedules fill up

Coworkers call dibs

Are Employee Stock Purchase Plans Underrated?

Why Employee Stock Purchase Plans can be a hidden gem - offering discounted stock and smart lookbacks.

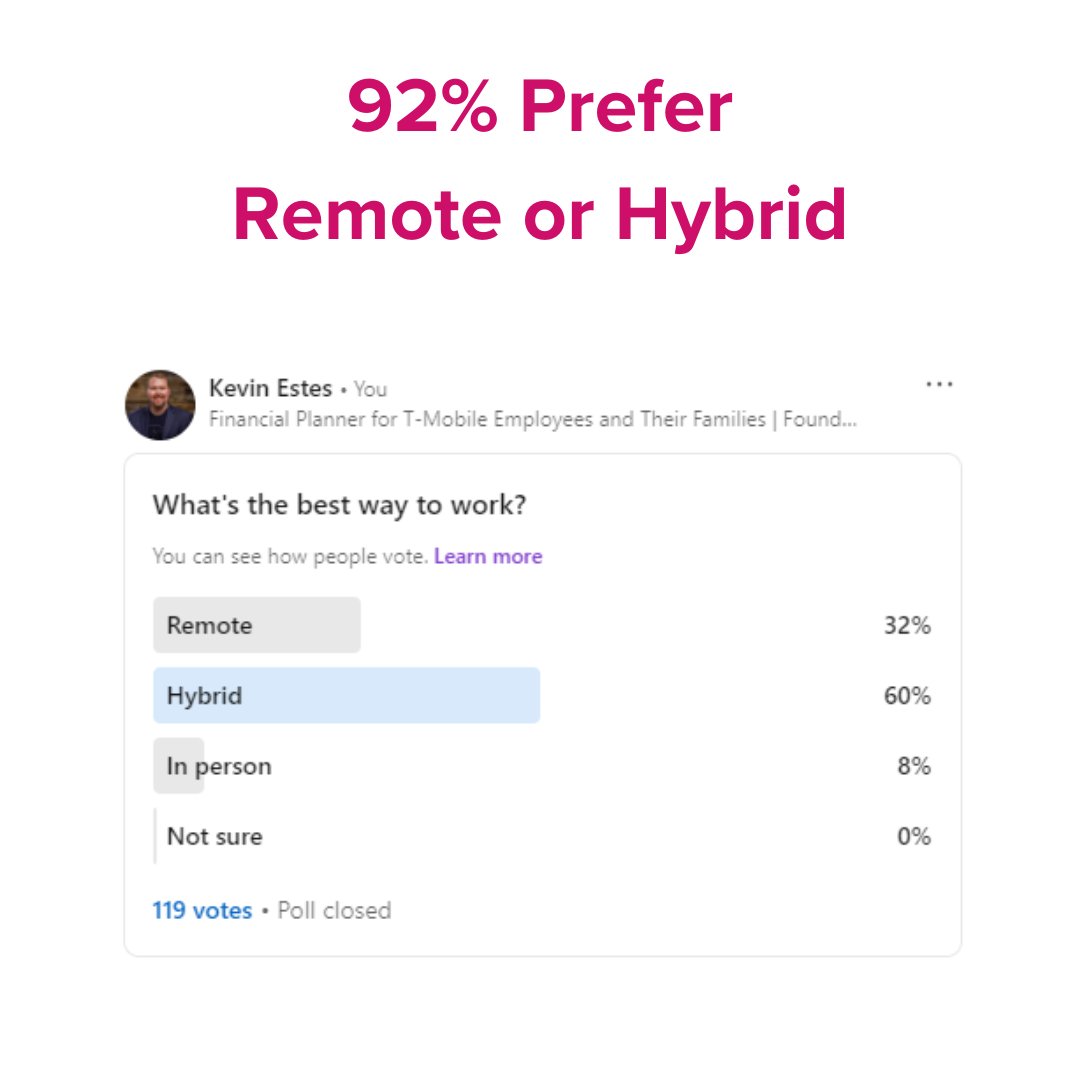

92% Prefer Remote or Hybrid

Unpack why 92% prefer remote or hybrid work - and how that matters for your financial priorities, flexibility, and lifestyle.

Is It Worth Holding Employer Stock?

There are risks of holding your employer’s stock - lack of diversification, it might not be as unique as it seems, and potential impacts to your other assets.

Big Takeaways from XYPN Live 2023!

I had the great fortune to attend the XYPN Live last week.

Michael Kitces asked me about my big takeaways.

They were all about mindset:

Stephanie Bogan’s challenge to think bigger

Michael Kitces’ closing keynote on scaling

Adam Cmejla’s perspectives on growth and automation

Do You Have the 3 T’s to Manage Finances Well?

Do you have the 3 T’s to manage finances well?

Those are:

Time

Training

Temperament

Are You Less Behind Than You Think?

How compound growth - using the rule of 72 - reveals that you may be further ahead than you feel in your financial journey.

Could Waiting a Year Cost $140,000?

How delaying financial moves by a year could cost you nearly $140,000 over 40 years - due to compound growth.

5 Ways to Lower Taxes Besides Donations

Five smart ways to lower your taxable income - like pre-tax retirement accounts, HSAs, spousal IRAs, tax-loss harvesting, and share sales.

Can Volunteering Save Your Life?

How volunteering once led to a lifesaving health check - and how helping others can improve your wellbeing, too.

Are You Ignoring $900,000?

Why ignoring Social Security could miss nearly $900,000 in retirement income - and how timing your benefits wisely matters.

Buying a Car

Five smart car-buying steps - from knowing your alternatives and negotiating financing to staying energized and walking away if needed.

Vacation + Disaster = Adventure

Discover how a smoke-filled vacation turned into a heartwarming, flexible getaway - pivoting plans and savoring unexpected moments.

Never Finance a Toy

One of the best pieces of advice I received came on a boat in Northern Idaho.

Joe and Amber were trying to get Kyle to take out a loan and buy a boat together.

Kyle declined using four words I’ll never forget:

“Never finance a toy.”

Types of Spending

Discover the four types of spending - needs, entertainment, societal, and addiction - and how they impact your physical and psychological well-being.

My Goal? Help People Reach Financial Independence!

My goal? Helping you reach financial independence so you choose to work - not because you have to.