Combining Finances is Like a Dimmer Switch

Why combining finances isn’t all-or-nothing - it’s like a dimmer switch with infinite ways to blend autonomy, fairness, and goals.

How Are Restricted Stock Units Taxed?

Know how RSUs are taxed - why vesting counts as income, how your share basis works, and short- vs. long-term capital gains.

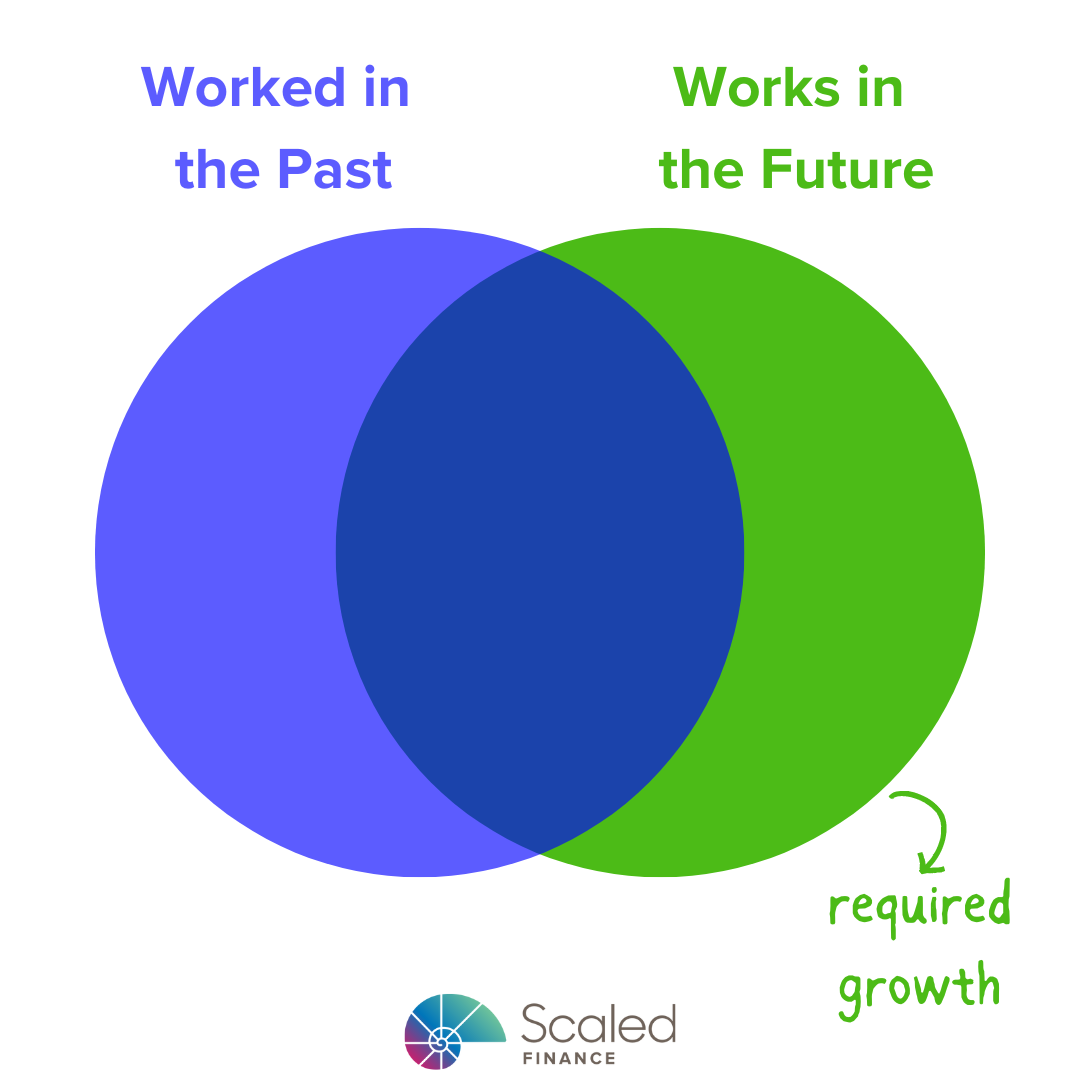

What Worked in the Past May Not Work in the Future

What worked in the past may not work in the future.

Change is like a current. Standing still takes effort. Making progress takes more.

Fortunately, most of life’s major changes happen every day!

Seek the counsel of those who have gone from where you are to where you want to go.

How Does a Couple Reach Financial Independence?

Know how couples may achieve financial independence: estimate expenses, subtract expected income, then multiply the shortfall by 25.

What Percent of Workers Max Social Security?

What percent of covered workers earn more than the Social Security maximum?

Only 6%!

It shocked me it was that low.

How about you?

What Is Financial Independence?

What is financial independence?

That’s the beauty of it. Everyone’s definition is different.

At its core, it's the ability to do what you like, when you like, and with whom you like.

Where We Focus vs. What Sinks Us

We tend to focus on what we know.

It’s specialization at its finest!

Unfortunately, this laser focus can create painful blind spots.

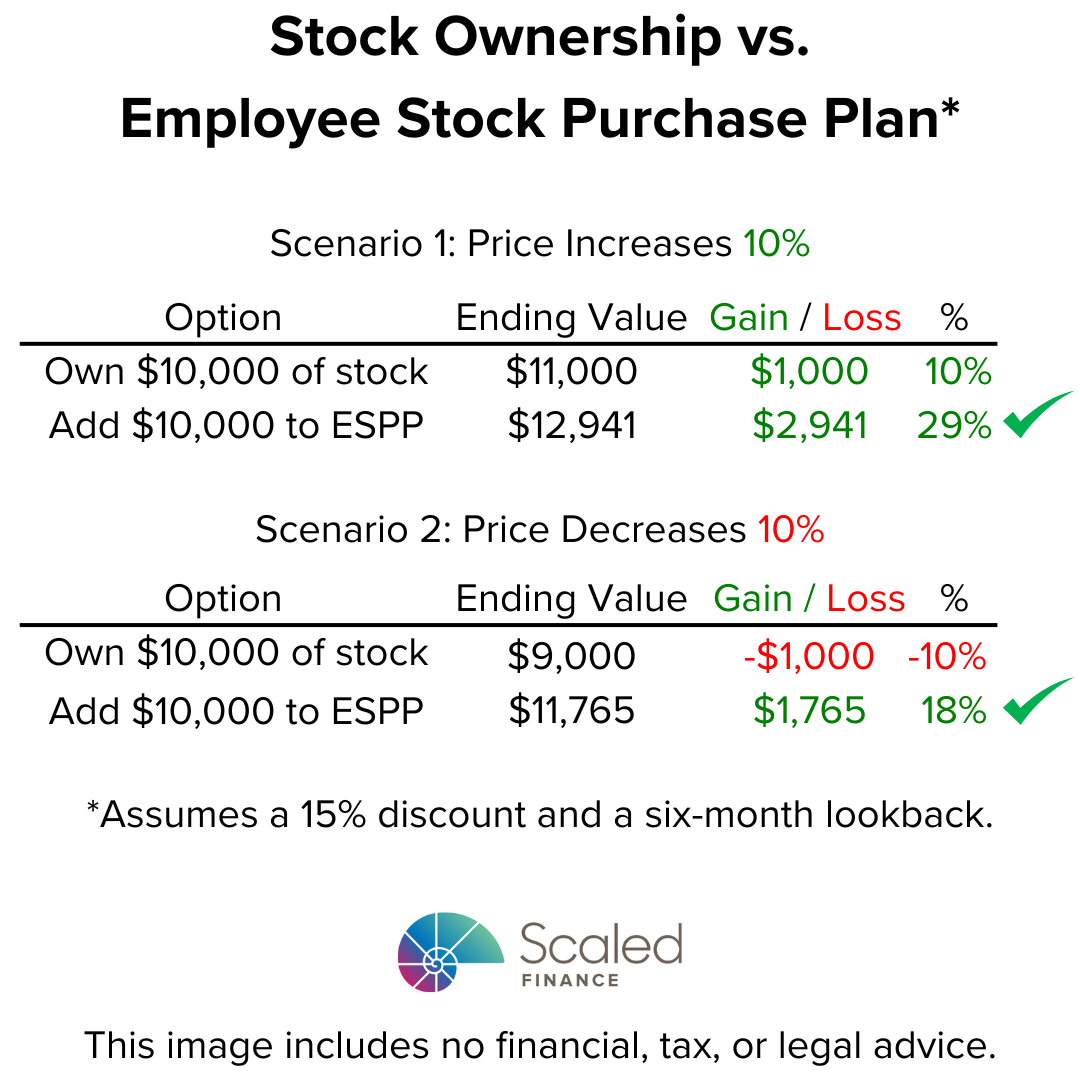

Own Stock or Contribute to ESPP?

Is it better to own stock or contribute to an Employee Stock Purchase Plan better?

Contributing to an Employee Stock Purchase Plan may be preferable.

Let’s compare a couple scenarios either:

owning $10,000 of stock or

contributing $10,000 to an Employee Stock Purchase Plan with a 15% discount and six month lookback

Scenario 1: a price increase of 10% could result in:

Ending value of $12,941 with the ESPP versus $11,000 if holding stock

Gain of $2,941 with the ESPP versus $1,000 if holding the stock

Return of +29% with the ESPP versus +10% if holding stock

Scenario 2: a price decrease of 10% could result in:

Ending value of $11,765 with the ESPP versus $9,000 if holding the stock

Gain of $1.765 with the ESPP versus loss of $1,000 if holding stock

Return of +18% with the ESPP versus -10% if holding stock