Frequent Restricted Stock Unit Vests May Be Win-Win-Win

How often Restricted Stock Units vest varies wildly from company to company. Shortening the time between vests may benefit companies, employees, and shareholders. However, employees stand to gain the most.

Sammy Says! 13 Things the U.S. Tax Code Encourages

Sammy Says! The U.S. Tax code encourages many things. Some of them include: 1. Get educated. 2. Get a job. 3. Earn some money. 4. Don’t make too much. 5. Pay medical expenses. 6. Get married. 7. Buy a home. 8. Go green. 9. Have or adopt children. 10. Invest long-term. 11. Save for retirement. 12. Give some away. 13. Don’t get too rich.

Love Future You

You know who could use some love? Future you! Many people receive their annual raise and bonus this time of year, making now a prime time to increase saving.

Potential Financial Steps for T-Mobile Employees in February

What financial steps might T-Mobile employees take in February? Options might include: update saving for raise and bonus, schedule tax prep meeting, gather tax forms and create checklist, accept Restricted Stock Units and grant, and review / rebalance investment portfolio.

Ignoring the Spousal IRA?

One of the most often overlooked opportunities is the spousal IRA. A spousal IRA is a traditional retirement account a spouse can contribute to despite earning little or no income. Contributing to a spousal IRA may help a couple lower their taxable income, reduce their taxes, and save for retirement.

Your Last Career Will Be Investor

When I was in high school, a mentor told me something that stuck: "No matter what you do, your last career will be investor." Three of the many reasons to learn how to invest include: 1. No one cares about your money as much as you. 2. You know yourself best. 3. It costs a lot to have someone manage investments.

Money and Freedom on MLK Day

A part of Dr. King’s “I Have a Dream” speech that resonates with me is early on when he uses debt as a metaphor for human rights. It’s beautiful how he articulates that the lack of freedom is a debt owed by the U.S. government to all Americans. I often equate money with freedom. However, I find the “Earn More!” / “Spend More!” debate comical. Do both! The forces amplify!

Investing in or Betting on Real Estate?

I know many people betting on real estate. They’re not investing! What’s the difference? Profitability. Someone's home is not an investment. It's a lifestyle! If it were an investment it'd be crazy expensive. This article explores these and many other real estate misconceptions as well as frameworks.

2023 Year in Review

2023 was a busy year! Inflation started hot and has since cooled. There were widespread tech layoffs. The S&P 500 returned 26.3% for the year. Billions in student loans were forgiven. Revenge spending included international travel and over $1,000 concert tickets.

Do You Even Need a Budget?

Do you even need a budget? I don’t budget. My wife and I evaluate expenses and then forecast. We do so for a bunch of reasons, including: a desire not to see expenses yo-yo with a restrictive budget, an opportunity to challenge every expense, and the ability to intentionally build the life we want.

Is Your Cash Starving?

I often meet people who keep way too little cash. They have great incomes - $100,000, $300,000, $500,000 a year, or more! However, they feel poor. Fortunately, many of them have significant investments! Having enough cash is like having good shocks. There are still bumps in the road. They just hurt less.

No Tax on Investment Gains?

Someone might pay no tax after selling an investment for a gain. There is a 0% capital gains tax bracket. However, it is very common for someone to pay a 15% capital gains tax.

Are My Assets in the Right Location?

I often see portfolios where every account is diversified! Such a portfolio is unnecessarily complex… and may not even be diversified although the investor thinks it is! For instance, someone with a heavy concentration of employer stock may own even more of it in their many target date, S&P 500, and sector funds!

5 Great Questions to Ask Yourself

What are five great questions to ask yourself? 1) What do I want my money to accomplish? 2) How do I minimize lifetime taxes? 3) What if I’m injured? 4) How can education costs be reasonable? 5) Are my assets in the right location?

Happy Thanksgiving!

Happy Thanksgiving, all!

I have even more than usual to be thankful for this year - including family, health, time, clients, and support.

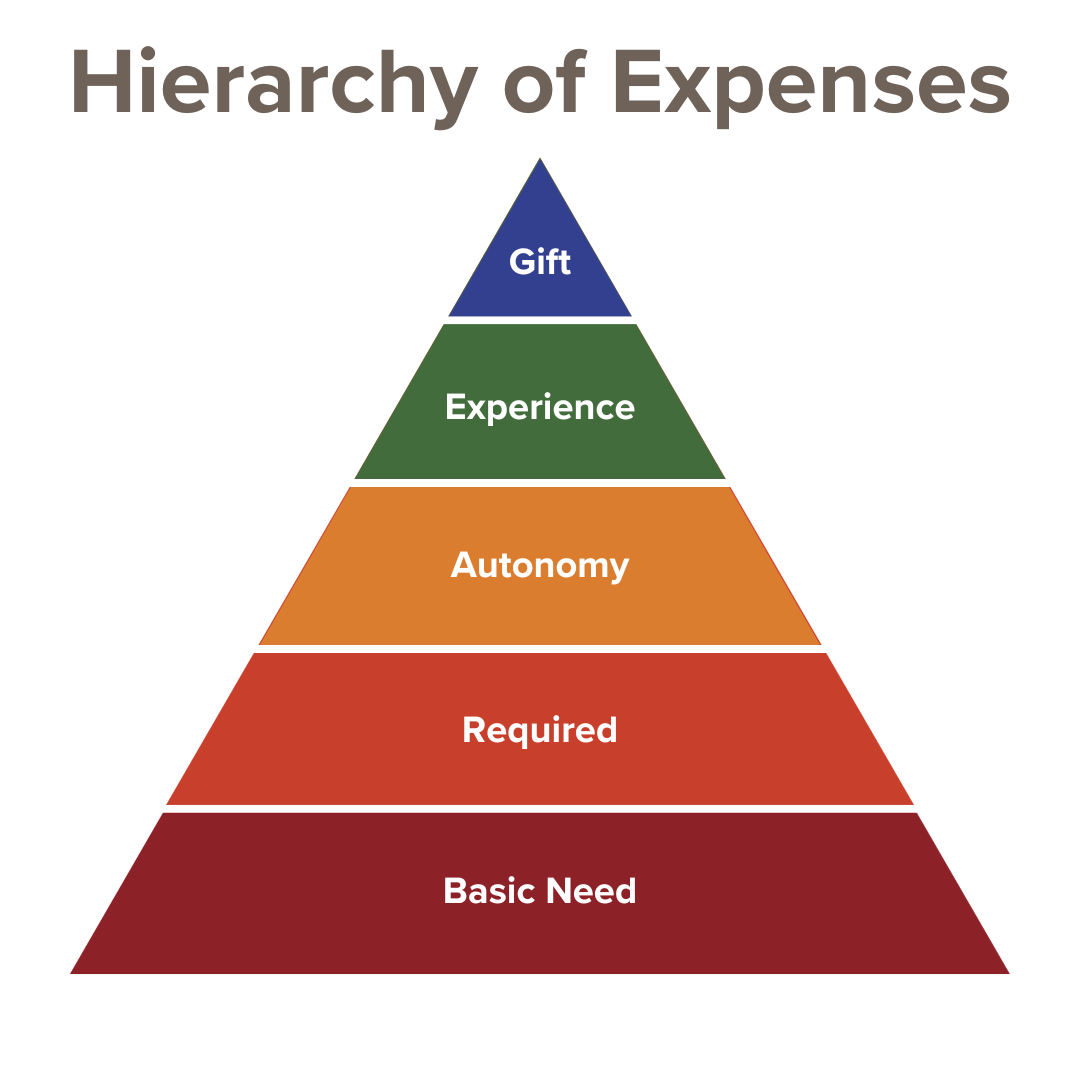

Hierarchy of Expenses

What are the hierarchy of expenses? Basic needs, required, autonomy, experience, and gift.

This article explores each in turn.

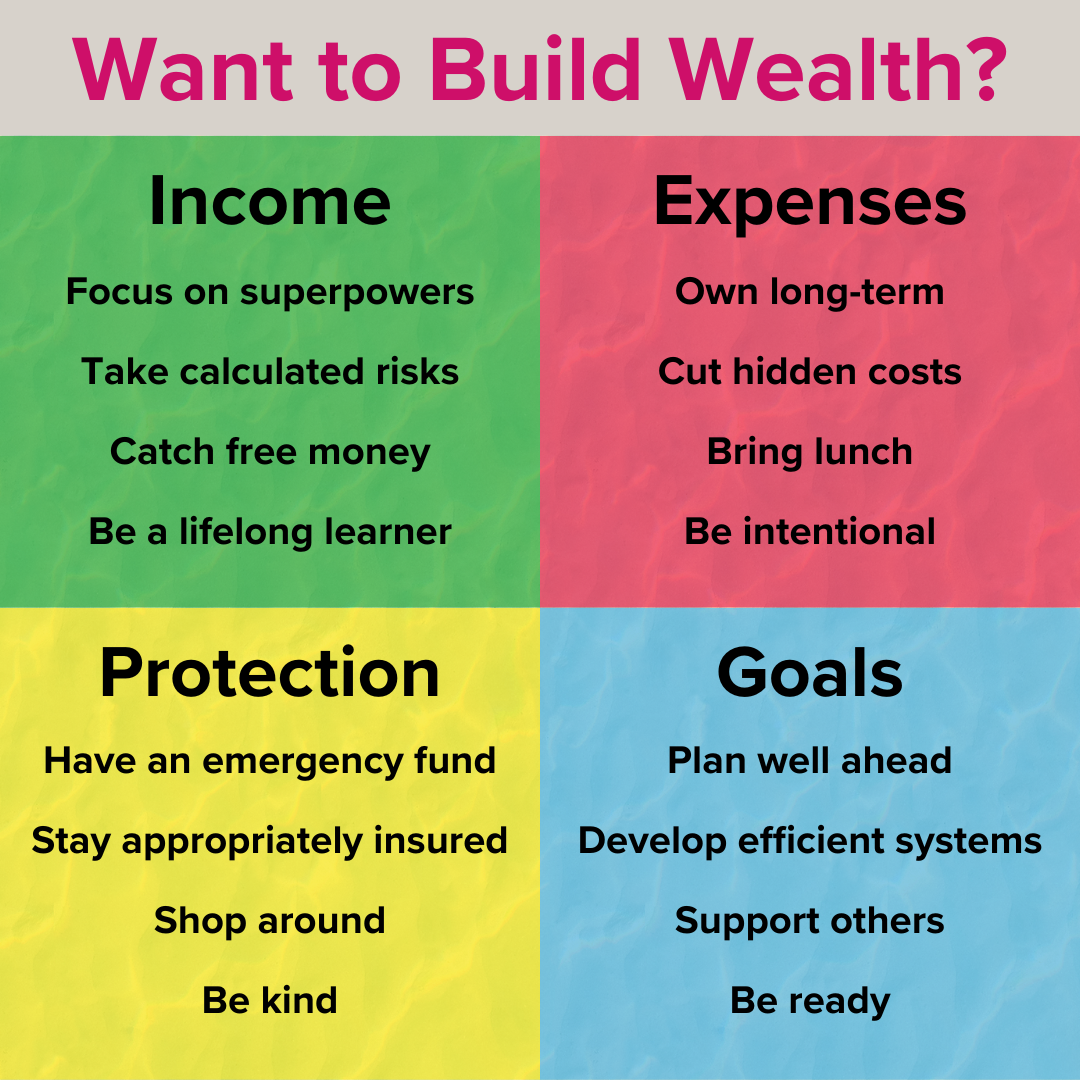

16 Ways to Build Wealth

Want to build wealth? Here are 16 ideas!

Income: focus on superpowers, take calculated risks, catch free money, and be a lifelong learner.

Expenses: own long-term, cut hidden costs, bring lunch, and be intentional.

Protection: have an emergency fund, stay appropriately insured, shop around, and be kind.

Goals: plan well ahead, develop efficient systems, support others, and be ready.

Benefit from Inertia

How could you benefit from inertia?

There’s a powerful force called static friction. It takes more effort to get something moving than to keep it moving.

This concept applies to many things, including: scheduling Paid Time Off (PTO), contributing to retirement plans, saving raises, and the like!

Pros and Cons of a Health Savings Account

It’s fall and you know what that means. It’s open enrollment season!

With open enrollment comes questions on Health Savings Accounts, or HSAs.

A Health Savings Account is a tax-advantaged way to save money for qualified medical expenses. Funds can be invested and grow for the future.

The biggest benefit of a Health Savings Account is its triple tax advantage. It:

• avoids tax on the front-end,

• grows tax-free, and

• can be withdrawn tax-free if used for qualified medical expenses.

The biggest drawback is that to contribute to an HSA, someone needs to be on a High Deductible Health Plan, or HDHP.

How Disability Insurance Works

Disability insurance is critical early in careers. After all, that's when we have the most future earnings to lose!

It's usually based on a percentage of income:

• 60% is somewhat standard, though

• it can range from 40 to 70%.

There's often a cap, which may cause higher earners to receive less than half their regular income.

There's short-term and long-term disability insurance:

• Short-term: first 3-6 months, typically own occupation coverage

• Long-term: after 3-6 months, often any occupation