Ignoring the Spousal IRA?

Hello, I’m Kevin - a financial planner who helps tech professionals and their families live great lives.

Make yourself at home - we’ll get the spousal IRA in a moment.

But first - here are some links you may want to save for later.

Contribute to Pre-Tax or After-Tax?

I Changes Jobs. Should I Roll Over My 401(k)?

Now, let's get on to the blog! 😀

What’s a Spousal IRA?

A spousal IRA is a traditional retirement account a spouse can contribute to despite earning little or no income.

It’s an often overlooked retirement account.

Contributing to a spousal IRA may help a couple:

lower their taxable income

reduce their taxes

save for retirement

One spouse may earn a high income while the other doesn’t. Given the cost of childcare, it’s especially common for families with children.

One spouse may:

work a part-time job or

dedicate themselves to managing the household.

People Assume They’re Not Eligible

Couples with income over $100,000 often assume they can’t benefit from these accounts.

It mostly depends on whether the spouse is covered by a retirement plan at work.

No Income

If a spouse doesn’t earn income, they’re probably not covered by a workplace plan.

However unlikely, it’s possible a former employer may continue to make retirement plan contributions on their behalf!

Little Income

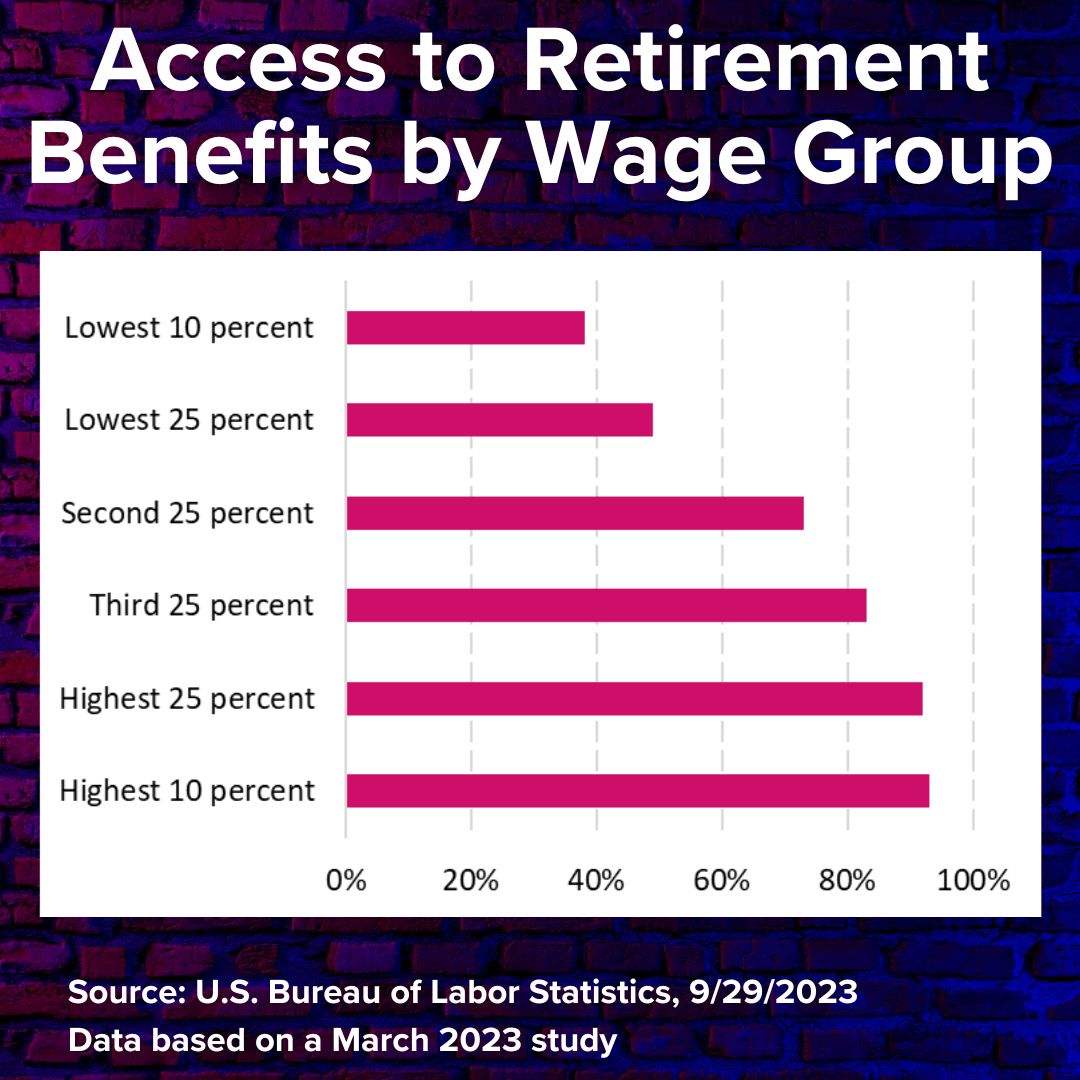

Lower wage and part-time positions have less access to retirement plans.

According to a study done in March 2023 by the U.S. Bureau of Labor Statistics, civilian access to retirement benefits varies by income:

Someone with a wage in the top 10% is about two and a half times more likely to have access to workplace retirement benefits than someone in the bottom 10%! 😮

If someone wanted to reduce wealth inequality, this seems like a good place to start.

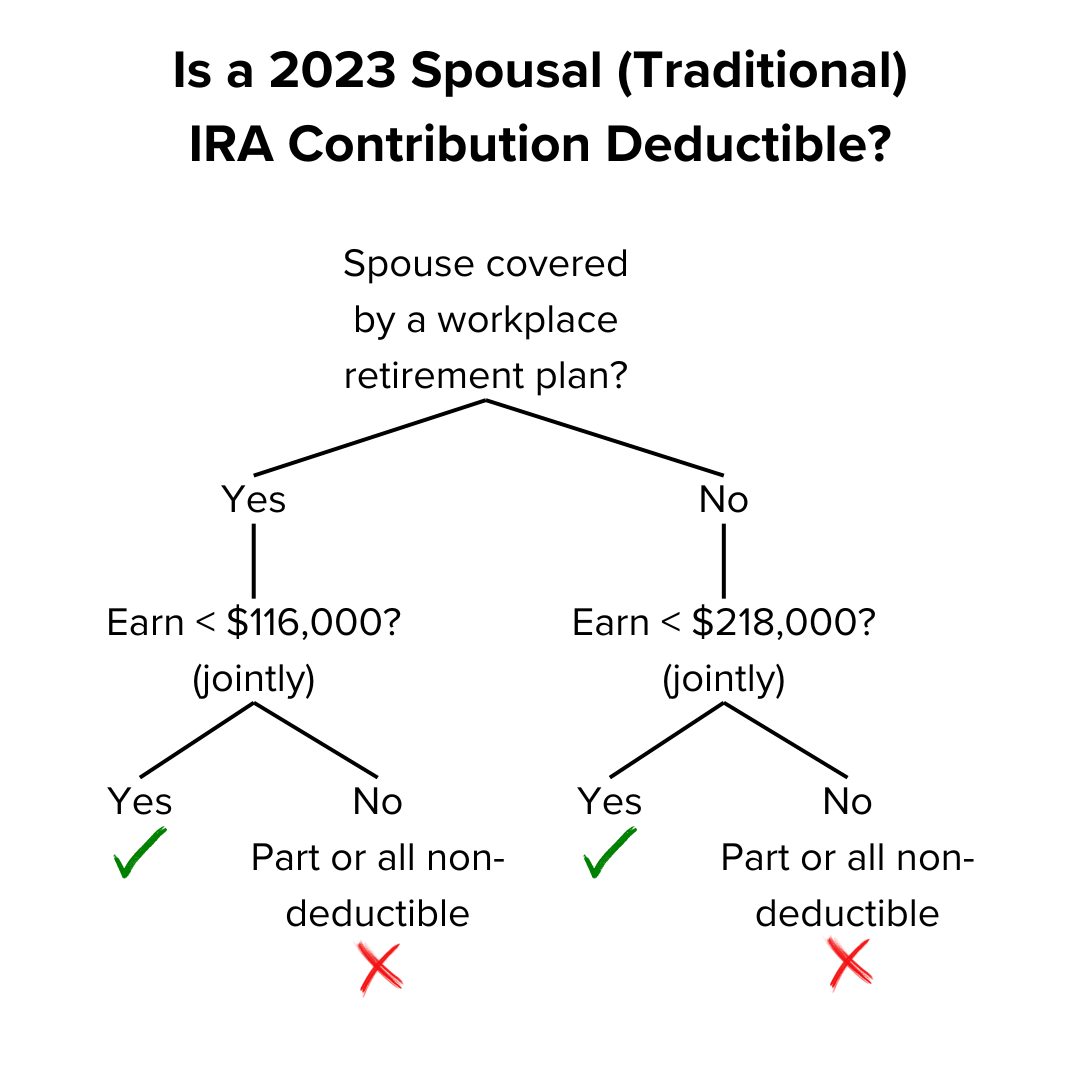

Are Spousal IRA Contributions Deductible?

Whether a spousal IRA contribution will reduce taxable income depends on:

whether the spouse is covered by a retirement plan at work

how much the married, filing jointly couple earns

Spouse Covered by a Retirement Plan at Work

The married filing jointly income limit if the spouse is covered by a retirement plan at work is:

2023: $136,000, and it’s phased out starting at $116,000

2024: $143,000, and it’s phased out starting at $123,000

Spouse NOT Covered by a Retirement Plan at Work

The married filing jointly income limit if the spouse is NOT covered by a retirement plan at work is:

2023: $228,000, and it’s phased out starting at $218,000

2024: $240,000, and it’s phased out starting at $230,000

The income used for these limits is Modified Adjusted Gross Income (MAGI).

Income Requirement

Wait, wouldn’t the spouse need earned income?

Nope! As long as the working spouse has enough income to cover their retirement plan contributions AND those of their spouse, they’re fine.

Let’s say someone earns $200,000. Their spouse takes care of their two young children and doesn’t have earned income.

No problem! The stay at home dad could still contribute to a traditional IRA and get a deduction on their joint tax return.

The maximum 401(k) employee contribution in 2023 was $22,500. That leaves $177,500 ($200,000 - $22,500) to contribute to the traditional IRA.

That Was So Last Year

Why do you keep talking about 2023?

Trust me. I didn’t celebrate the New Year so hard that I forgot it happened!

A cool thing about IRA contributions? Americans have until their tax filing deadline to contribute for the previous year.

A 2023 contribution can be made up to 4/15/2024!

A couple might still be able to grow their retirement account(s) and their upcoming tax refund. They would need to specify 2023 for the traditional IRA contribution.

Account Ownership

Who owns the account?

The “Individual” in “Individual Retirement Arrangement” matters. They aren’t owned jointly.

Regardless of who contributes funds to the account, the person whose name is on the account owns it.

Age Is Irrelevant

Isn’t there a limit on how old someone can be and contribute to an IRA?

Not anymore!

The limit used to be 70.5. However, that limit was removed for 2020 and later.

There also isn’t a minimum age requirement. A teen who works a summer job could contribute (or have a parent contribute) to their Roth or traditional IRA account!

Contribution Limits

Isn’t the amount that can be contributed low?

The maximum contribution for traditional (and Roth) IRA for those 50 years old and younger is:

Someone who’s at least 50 years old can make an extra $1,000 catch-up contribution.

True - that’s far below the employee 401(k) contribution limit of:

However, it’s well above the individual limits for another attractive option - the Health Savings Account (HSA):

Roth vs. Traditional

As good as the traditional IRA is, there may be a better option in some situations.

Unlike traditional IRA contributions, Roth contributions don’t lower taxable income for the year they’re made.

However, funds withdrawn from a Roth IRA aren’t taxed if criteria are met.

Lowers Taxable Income the Year Contributed

With a traditional IRA, contributions generally lower taxable income for the year. However, they won’t be deductible if income exceeds the limits.

Roth IRA contributions don’t reduce taxable income in the year they’re made.

Grows Tax Advantaged

Fortunately, neither traditional nor Roth IRA accounts are taxed annually:

Traditional IRA accounts typically grow tax-deferred

Roth IRA accounts typically grow tax-free

This saves on both the hassle and tax cost. In addition, interest and dividends earned in those accounts are reinvested. They may start to grow exponentially!

Two major exceptions are:

required minimum distributions and

inheritance.

We’ll explore those later.

Withdrawals are Tax-Free

Because the Roth IRA account owner paid taxes on the front end, they may never be taxed again! Withdrawals will be tax-free if certain requirements are met.

A common metaphor is a fruit tree. Is the seed or fruit taxed?

With a traditional IRA, the seed is not taxed yet the fruit is.

It’s the opposite for a Roth IRA. The seed is taxed and the fruit isn’t.

Roth IRA withdrawals come out in the following order:

Contributions - can be withdrawn tax and penalty free at essentially any time.

Conversions - generally need to be withdrawn at least five years after they’re converted and after someone turns 59.5.

Earnings - would be taxed if withdrawn either less than five years after the account was funded or before age 59.5.

Unless an exception is met, a 10% penalty would apply if contributions and/or earnings are withdrawn before age 59.5. The same penalty applies to early traditional IRA withdrawals.

Requires Minimum Distributions (RMDs)

The U.S. Government gets impatient with traditional IRAs. Someone received a tax break year or even decades ago.

It’s time to pay!

Many people would prefer to never take money out of their traditional IRA accounts. The IRS forces them to with Required Minimum Distributions (RMDs).

The government would prefer to have traditional IRA owners distribute their entire balance before they die.

How much must be withdrawn each year is based on age. The older someone is, the larger the percentage they must take out each year. It’s based on life expectancy tables.

People are now living longer. Fortunately, the age someone must start taking Required Minimum Distributions (RMDs) has also increased.

The current age is 72.

However, it’s planned to rise to 75 by 2033.

Typically, people subject to Required Minimum Distributions (RMDs) have done well. They don’t really need to use these retirement accounts to fund their living expenses.

Roth IRAs aren’t subject to annual Required Minimum Distributions.

That makes sense! The government received its taxes years ago.

Roth Use Cases

There are many potential scenarios for Roth IRA contributions, including:

Income Expected to Rise: Younger workers tend to earn less than they will later. Since tax rates are progressive, it may make sense to pay the taxes now instead of later.

No State Income Tax: Earners who live in an income tax free state like Texas or Washington and plan to move might be ahead to pay the income taxes now. Doing so could avoid state income taxes later!

Inheritance: If someone were to leave a traditional IRA to a family member when they pass, that person would have to pay income taxes! The timing could be especially bad if the heir is in their peak earning years. Inherited Roth IRA aren’t really subject to income taxes.

Other Cash Needs

Someone needs to be able to contribute to an IRA.

Other things which often take priority include:

living expenses - including child support and alimony

taxes - especially back taxes

high interest credit debt

business expenses

emergency fund

insurance premiums

matched retirement plan contributions

discounted stock purchases…

Everyone’s situation is unique.

Must Be Eligible

This assumes the couple can contribute to a Roth IRA!

Unlike with a traditional IRA, the limits don’t depend on whether the spouse is covered by a retirement plan at work. What matters is the couple’s income.

The Roth IRA income limits for a married couple filing jointly are:

2023: $228,000, and it’s phased out starting at $218,000

2024: $240,000, and it’s phased out starting at $230,000

It’s Worth Checking

Even if previously unable to contribute to a Roth IRA or deduct a traditional IRA contribute, it’s worth checking. Things change!

Hey, thanks for reading my post on the spousal IRA.

Just a reminder, I share a lot of resources that can help you.

Disclaimer

In addition to the usual disclaimers, neither this post nor this image includes any financial, tax, or legal advice.