Are My Assets in the Right Location?

I often see portfolios where every account is diversified! Such a portfolio is unnecessarily complex… and may not even be diversified although the investor thinks it is! For instance, someone with a heavy concentration of employer stock may own even more of it in their many target date, S&P 500, and sector funds!

5 Great Questions to Ask Yourself

What are five great questions to ask yourself? 1) What do I want my money to accomplish? 2) How do I minimize lifetime taxes? 3) What if I’m injured? 4) How can education costs be reasonable? 5) Are my assets in the right location?

Happy Thanksgiving!

Happy Thanksgiving, all!

I have even more than usual to be thankful for this year - including family, health, time, clients, and support.

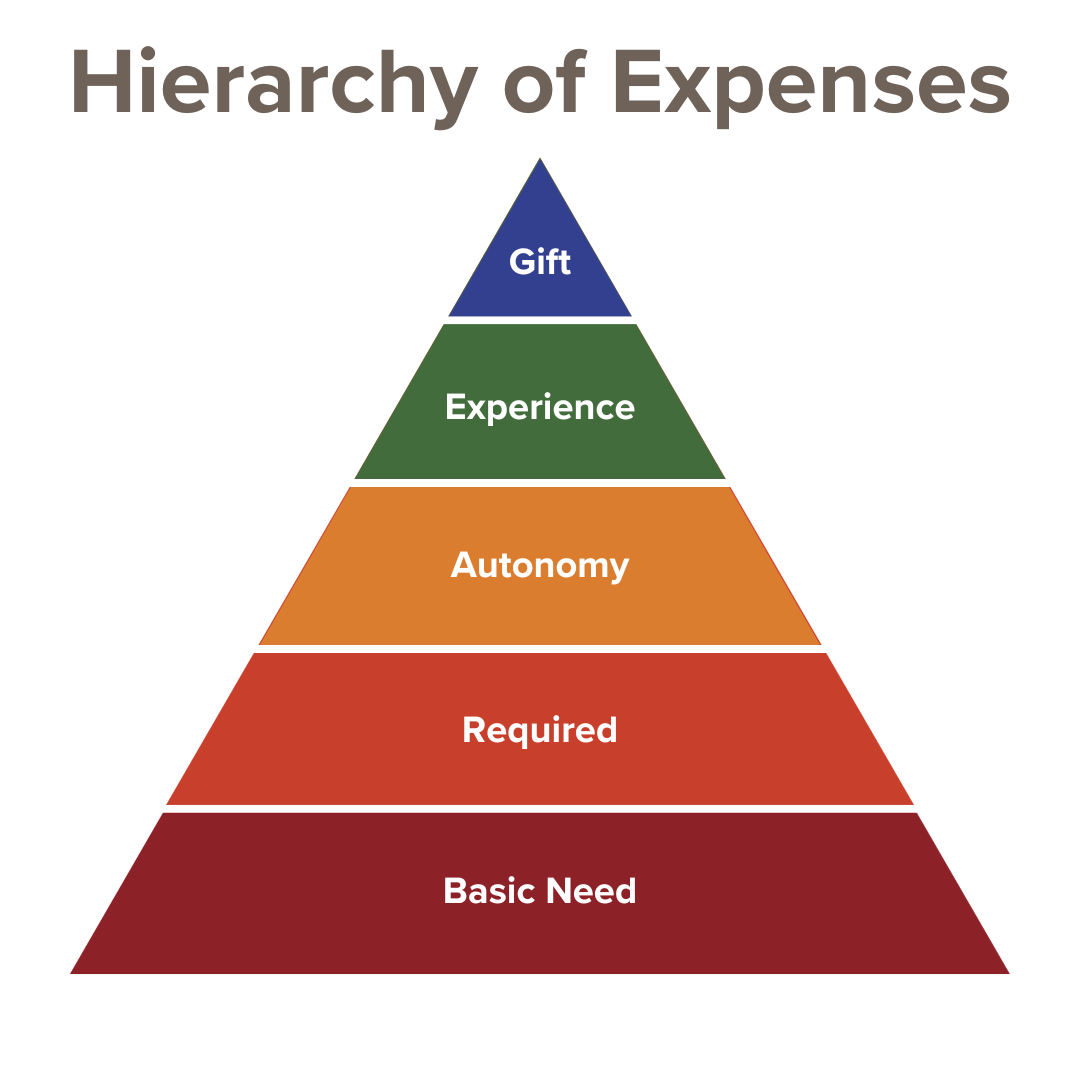

Hierarchy of Expenses

What are the hierarchy of expenses? Basic needs, required, autonomy, experience, and gift.

This article explores each in turn.

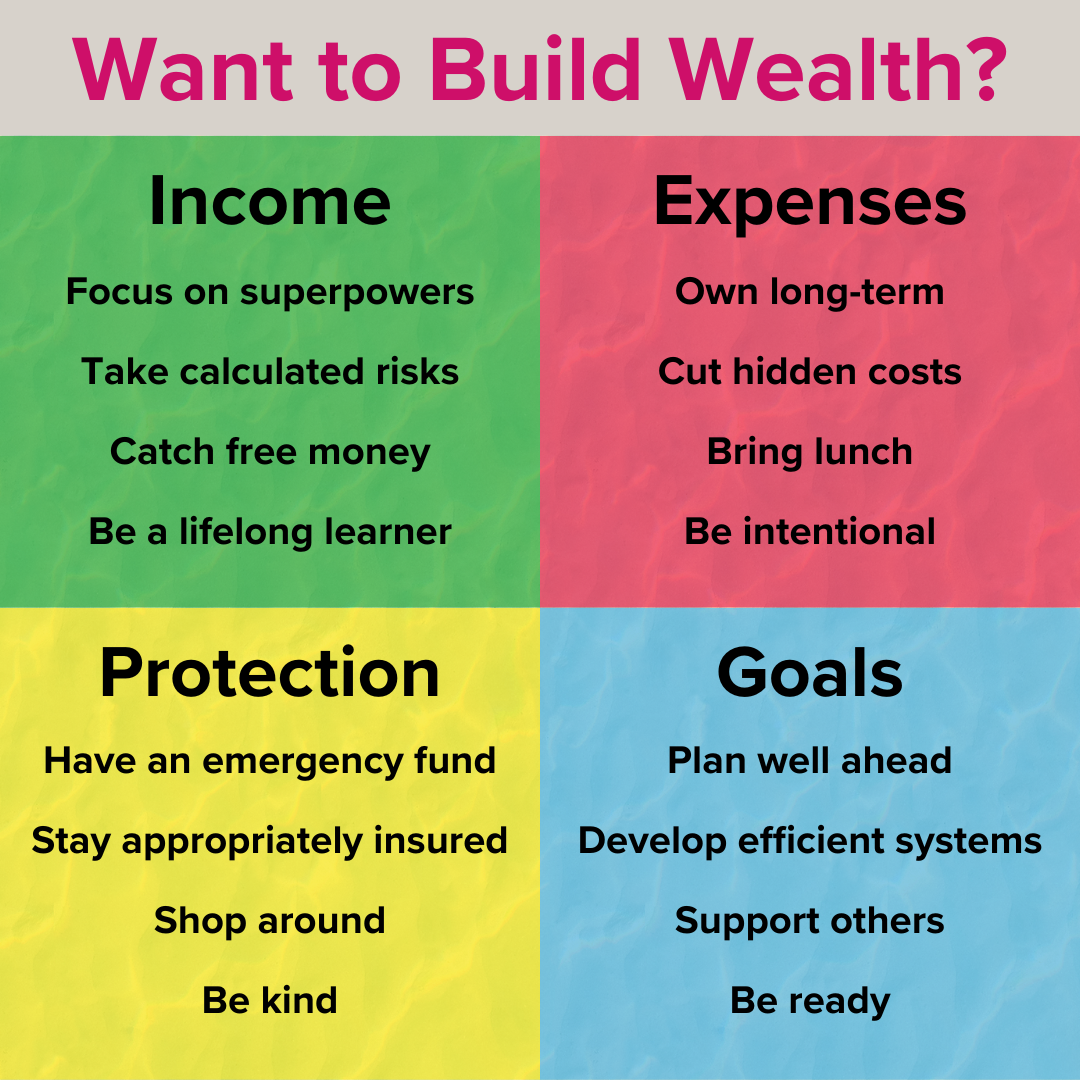

16 Ways to Build Wealth

Want to build wealth? Here are 16 ideas!

Income: focus on superpowers, take calculated risks, catch free money, and be a lifelong learner.

Expenses: own long-term, cut hidden costs, bring lunch, and be intentional.

Protection: have an emergency fund, stay appropriately insured, shop around, and be kind.

Goals: plan well ahead, develop efficient systems, support others, and be ready.

Benefit from Inertia

How could you benefit from inertia?

There’s a powerful force called static friction. It takes more effort to get something moving than to keep it moving.

This concept applies to many things, including: scheduling Paid Time Off (PTO), contributing to retirement plans, saving raises, and the like!

Pros and Cons of a Health Savings Account

It’s fall and you know what that means. It’s open enrollment season!

With open enrollment comes questions on Health Savings Accounts, or HSAs.

A Health Savings Account is a tax-advantaged way to save money for qualified medical expenses. Funds can be invested and grow for the future.

The biggest benefit of a Health Savings Account is its triple tax advantage. It:

• avoids tax on the front-end,

• grows tax-free, and

• can be withdrawn tax-free if used for qualified medical expenses.

The biggest drawback is that to contribute to an HSA, someone needs to be on a High Deductible Health Plan, or HDHP.

How Disability Insurance Works

Disability insurance is critical early in careers. After all, that's when we have the most future earnings to lose!

It's usually based on a percentage of income:

• 60% is somewhat standard, though

• it can range from 40 to 70%.

There's often a cap, which may cause higher earners to receive less than half their regular income.

There's short-term and long-term disability insurance:

• Short-term: first 3-6 months, typically own occupation coverage

• Long-term: after 3-6 months, often any occupation

Happy National Boss’s Day!

Who have your best managers been?

What made them great?

I’ll start! Some of mine were:

Tony Russo

Gary Austin

Thushan Wijesinghe

Orna Samuelly

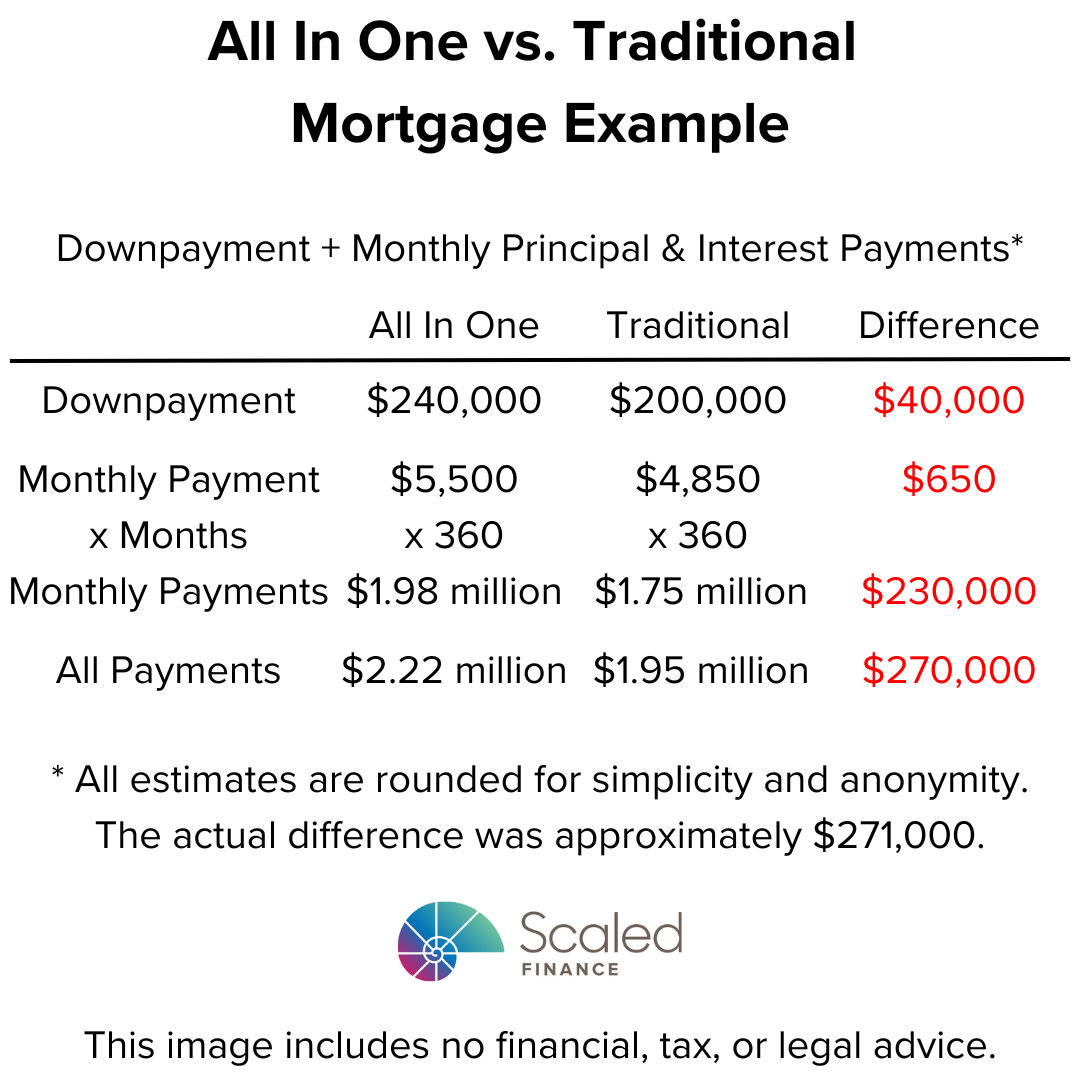

Could an All In One Mortgage Cost an Extra $270,000?

A first-time homebuyer I met was excited about an all in one mortgage.

Comparing apples to apples, the all in one mortgage would cost an additional $270,000 over the life of the loan:

~$40,000 higher downpayment

~$650 higher monthly payment

Charge Market Rent!

Many clients who own investment real estate undercharge for rent.

Few things can improve profitability and cash flow like a reasonable price increase.

A change may lift profitability for as long as someone owns the home. It also raises the value of the property for investors looking to buy!

Charging below market isn't doing tenants any long-term favors.

Schedule Your PTO ASAP

Schedule your Paid Time Off (PTO) as soon as possible!

Lodging gets booked

Flight prices rise

Schedules fill up

Coworkers call dibs

Are Employee Stock Purchase Plans Underrated?

An Employee Stock Purchase Plan (ESPP) is a way to leverage employer stock with less risk.

Many plans include both a discount a lookback. The lookback feature takes the lower of the price at the beginning and end of the offering period.

Some important considerations with Employee Stock Purchase Plans (ESPP) include:

• They don't all work the same.

• Participating in a plan isn't for everyone.

• It's critical to use Form 3922 to avoid double taxation on the contributions.

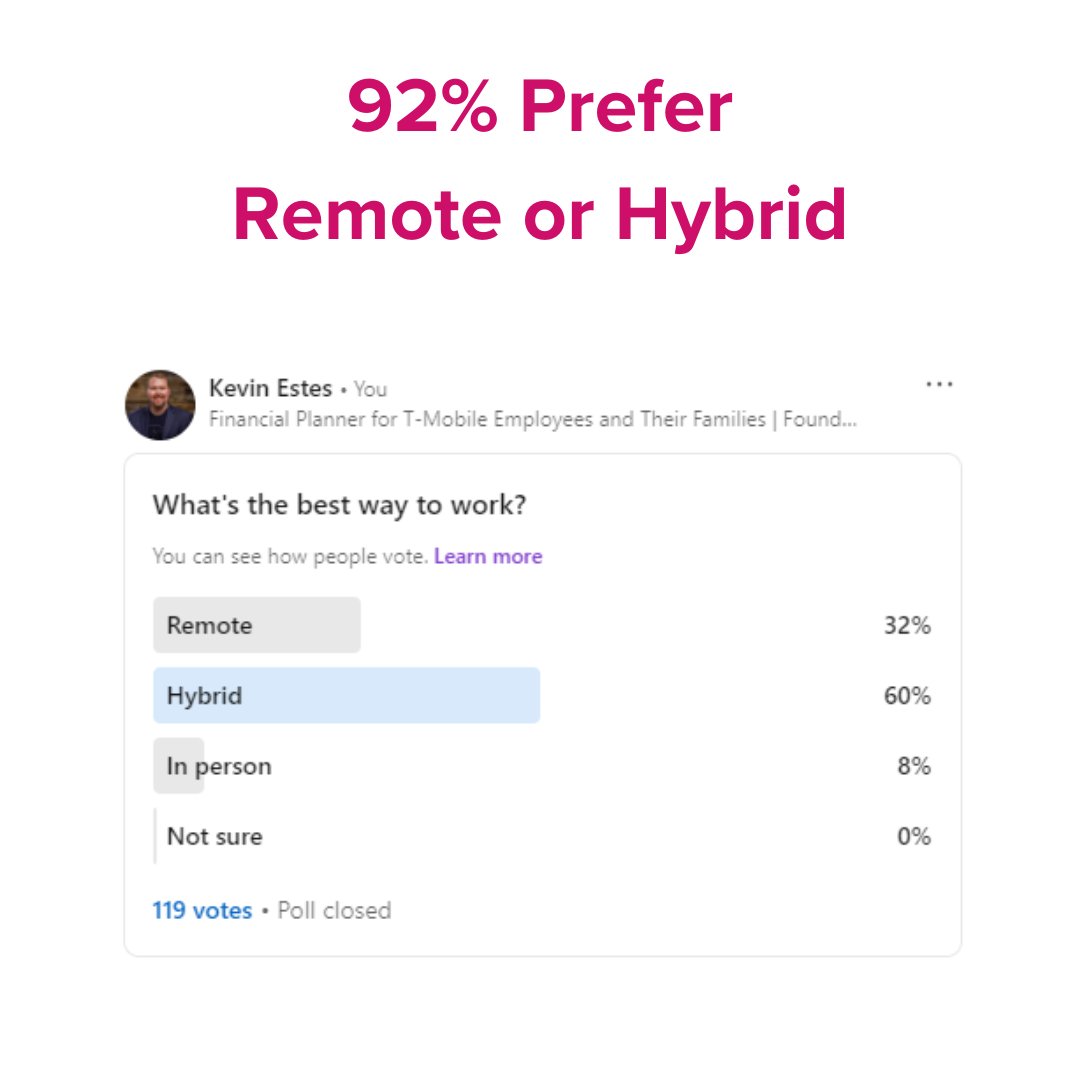

92% Prefer Remote or Hybrid

The results of a recent LinkedIn poll were fascinating.

“What’s the best way to work?”

32% Remote

60% Hybrid

8% In person

0% Unsure

Is It Worth Holding Employer Stock?

One thing that often comes up in client conversations is whether to hold employer stock. It's understandable to want to keep company shares!

Holding employer stock might not be ideal because: an employee has a lot riding on the company; one stock has greater risk than the overall market; and employees are often already rewarded for company stock performance.

Big Takeaways from XYPN Live 2023!

I had the great fortune to attend the XYPN Live last week.

Michael Kitces asked me about my big takeaways.

They were all about mindset:

Stephanie Bogan’s challenge to think bigger

Michael Kitces’ closing keynote on scaling

Adam Cmejla’s perspectives on growth and automation

Do You Have the 3 T’s to Manage Finances Well?

Do you have the 3 T’s to manage finances well?

Those are:

Time

Training

Temperament

Are You Less Behind Than You Think?

Some people feel discouraged with their finances.

However, it’s not all doom and gloom!

Here’s where the “rule” of 72 comes in handy.

A 40 year old with $200,000 saved for retirement who expects to earn an 8% return might have:

$400,000 by age 49,

$800,000 by age 58, and

$1.6 million by age 67.

Could Waiting a Year Cost $140,000?

Many people put off financial planning.

However, optimizing finances early can be impactful!

With an 8% annual return, $500 a month turns into about:

$37,000 in five years,

$91,000 in 20 years,

$745,000 in 30 years,

and $1.75 million in 40 years.

5 Ways to Lower Taxes Besides Donations

5 ways to lower taxable income besides donations:

1. Pre-tax retirement accounts like 401(k), 403(b), and 457

2. Health Savings Account (HSA)

3. Spousal Individual Retirement Account (IRA)

4. Tax loss harvesting

5. Specifying which shares to sell if selling stock