Contribute to Pre-Tax or After-Tax?

Hello, I’m Kevin - a financial planner who helps tech professionals and their families live great lives.

Make yourself at home - we'll get to pre-tax and after-tax retirement plan contributions in a moment.

But first - here are some links you may want to save for later.

How to Minimize Lifetime Taxes

Transactions in Retirement Accounts Aren't Taxed... Yet

Now, let's get on to the blog! 😀

Plan Options

Many people struggle with whether to contribute to a pre-tax or after-tax plan. Both is also an option!

Pre-tax and after-tax options may exist for plans like:

401(k)

403(b)

457(b)

Individual Retirement Arrangement (IRA)

The pre-tax version may be called “traditional” whereas the after-tax version is often a Roth plan.

This article explores some important factors which may influence whether to contribute to pre-tax, after-tax, or both.

Pre-Tax and After-Tax Defined

The primary difference between a pre-tax and after-tax account is:

pre-tax = pay taxes later

after-tax = pay taxes now

Pre-tax accounts are also called “tax-deferred.”

Consider a fruit tree metaphor:

a pre-tax account avoids tax on the seed but not the fruit

an after-tax account is taxed on the seed but not the fruit

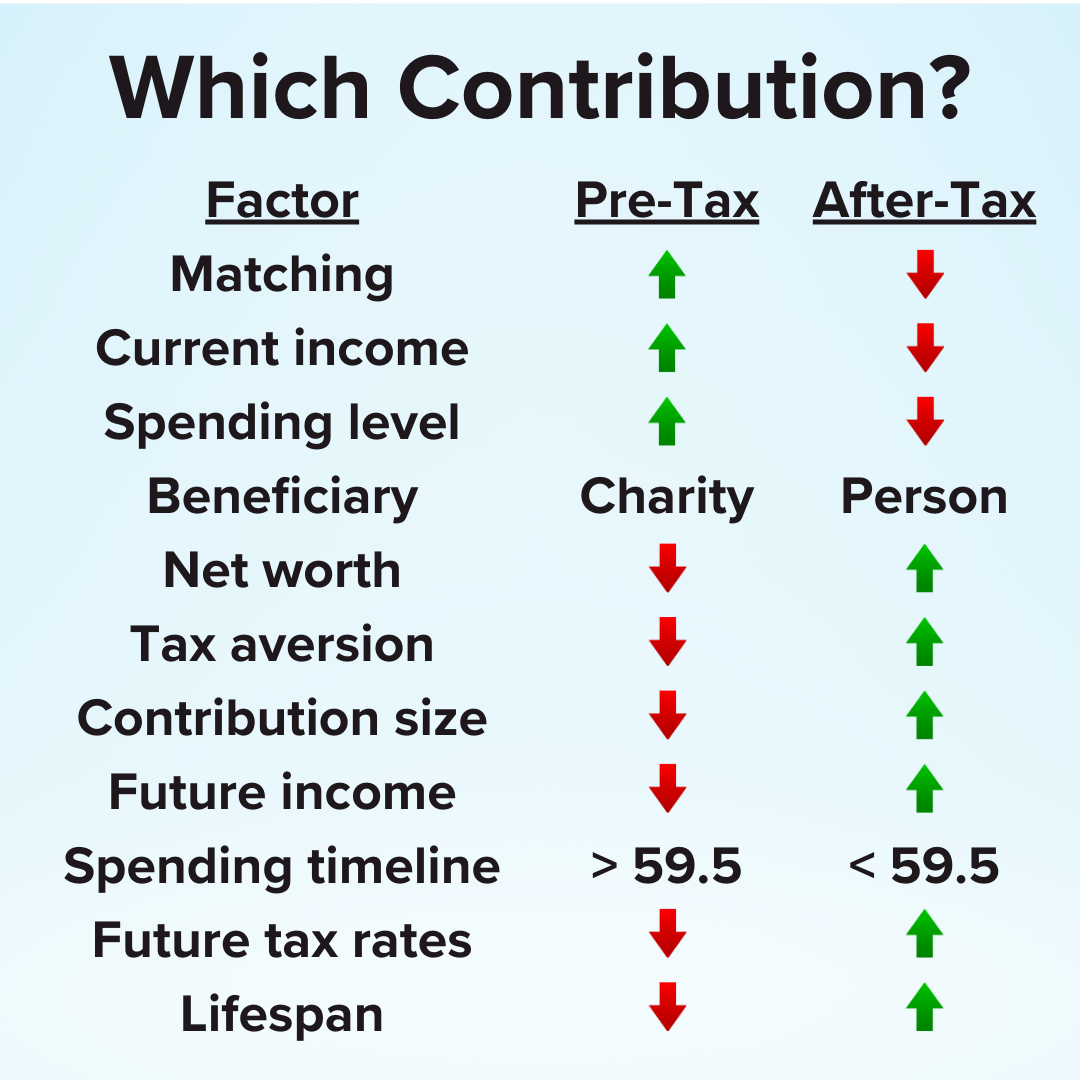

Important Factors

Many things influence the decision to contribute to a pre-tax or after-tax account.

Pre-tax contributions may be better for:

company matching

high current income

high spending

charitable giving

After-tax contributions may be better for:

high net worth

minimizing lifetime taxes

maximizing contributions

high future income

spending before age 59.5

high future tax rates

longer lifespans

Matching

Given the same cash flow, someone may be able to leverage the tax savings to contribute more.

Saving more could:

increase the company match and

maximize the Saver’s Credit.

Company Match

It’s more likely a pre-tax contribution will be matched by the employer.

Some employers don’t match after-tax contributions! In that case, it likely makes sense to contribute to a traditional (pre-tax) account.

Saver’s Tax Credit

The Saver’s Credit (also known as the Retirement Savings Contributions Credit) is available to those who earn up to the following in 2024:

$76,500 married, filing jointly

$57,375 head of household

$38,250 single

Current Income

It often makes sense for higher earners to make deductible contributions to pre-tax accounts. That’s because they can avoid a high tax rate now.

The tax impact depends on many factors like:

filing status,

other deductions/credits,

Alternative Minimum Tax,

Net Investment Income Tax, etc.

It can also depend on contribution and income limits.

Contribution Limits

Workplace retirement plans offer higher contribution limits and fewer deduction restrictions than Individual Retirement Arrangements (IRAs).

Employer Plan Contribution Limits

Contributions to a pre-tax 401(k), 403(b), 457(b), and the federal government’s Thrift Savings Plan lower taxable income.

The 2024 contribution limits are:

$23,000

plus a $7,500 catch-up for those at least 50 year old

IRA Contribution Limits

Individual Retirement Arrangements have lower contribution limits.

The 2024 contribution limits are:

$7,000

plus a $1,000 catch-up for those at least 50 years old

Income Limits

Higher earners may not be able to either:

deduct pre-tax IRA contributions or

contribute to a Roth IRA.

IRA Deduction Income Limits

Whether a pre-tax contribution can lower taxable income depends on:

filing status,

income, and

whether the worker is covered by a workplace retirement plan.

At least some of the pre-tax contribution is deductible up to income of:

$87,000 single

$143,000 married, filing jointly if covered by an employer plan

$240,000 married, filing jointly if not covered by an employer plan

Roth IRA Income Limits

A high earner may not be able to contribute directly to a Roth IRA.

At least some Roth IRA contributions can be made up to:

$161,000 for single and head of household filers

$240,000 for married couples filing jointly

Spousal IRA

A spouse with little or no income may be able to contribute to their own pre-tax (traditional) or after-tax (Roth) IRA.

Their spouse would need to earn enough to cover all of their contributions. The income limits for pre-tax deductions and Roth contributions above also apply to a spousal IRA.

For more, check out:

Are You Ignoring the Spousal IRA?

Spending Level

Tax savings can enable someone to contribute more pre-tax than after-tax. Larger contributions grow account balances more quickly.

A larger nest egg early on may better support more expensive lifestyles.

Healthcare Expenses

Healthcare is one of the most variable expenses in America.

Major Medical

Two of the few benefits of major expenses are that they’re:

generally deductible above 7.5% of Adjusted Gross Income and

That means there may be few tax impacts from using a pre-tax account to fund major healthcare expenses.

Someone who expects major medical expenses may be ahead to contribute to a pre-tax account. The available balance may grow larger without many tax consequences.

Health Savings Account

The sad irony of Health Savings Accounts (HSAs) is that those most likely to need them are least likely to have them.

Health Savings Accounts require someone to be on a qualifying High Deductible Health Plan (HDHP). People with significant ongoing healthcare expenses are more likely to reach their deductibles, which makes it less likely they’ll choose a HDHP.

However, someone already on a qualifying plan could receive a unique triple-tax advantage with Health Savings Account contributions:

avoid tax on the front-end,

grow tax-free, and

avoid tax if withdrawn for qualifying healthcare expenses.

Those contributions might avoid tax altogether!

It may make sense to prioritize HSA contributions over either pre-tax or after-tax contributions.

Also, someone with a significant Health Savings Account balance may be in a better position to contribute to an after-tax plan.

For more, check out:

Pros and Cons of a Health Savings Account

Long-Term Care

The cost of long-term care is high. Someone with a family history of dementia may risk years of heavy expenses late in life.

Having long-term care insurance lowers the risk of major expenses. Someone with long-term care insurance may be able to prioritize after-tax contributions.

Beneficiary

How someone plans to leave assets also influences whether to make pre-tax or after-tax contributions.

Charities

Nonprofits don’t pay income taxes. As such, they don’t care whether assets are pre-tax or after-tax.

If someone plans to leave their assets to charity, it may make sense to prioritize pre-tax contributions.

RMDs

Required Minimum Distributions can shrink pre-tax accounts because:

an amount is required to be withdrawn each year and

the account holder often has to pay tax on the income.

QCDs

Fortunately, there’s a solution: Qualified Charitable Distributions (QCDs). These are essentially Required Minimum Distributions the owner gives directly to charity.

The federal tax code allow Qualified Charitable Distributions to satisfy the Required Minimum Distributions without the account holder reporting or paying tax on that income. However, there are limits.

People

Although a charity might not care whether the assets are pre-tax or after-tax, an heir would!

That’s because the recipient has to report withdrawals as income. An heir essentially pays the tax the deceased didn’t!

Worse, the recipient may:

be in their peak earning years and

only have 10 years to withdraw the funds from the account.

Net Worth

Someone’s net worth could influence whether they contribute to a pre-tax or after-tax account.

Pre-Tax for Lower Net Worth

All else equal, a lower net worth is more likely to be spent during someone’s life.

Making pre-tax contributions can result in larger account balances early. That provides additional flexibility - especially if the expense is deductible such as a major medical expense.

After-Tax for Higher Net Worth

A higher net worth may enable someone to delay spending it until late in life - if ever.

That could:

give money longer to grow tax-free,

avoid Required Minimum Distributions, and

keep heirs from having to pay income tax on an inheritance.

Tax Aversion

If someone is opposed to paying taxes, it may make sense to make after-tax contributions.

Someone who lives sufficiently long will likely pay less in tax with an after-tax contribution. That’s because the seed is taxed, not the fruit.

Example

Let’s assume:

an employee is 40 years old

contributes annually for 20 years until age 60

pays a 24% marginal federal tax rate every year

lives in a state without income tax

earns an annual return of 7% on investments

starts Required Minimum Distributions at age 75

only uses the distributions to pay taxes

invests the rest in investments without taxable income (buy and hold growth stocks, municipal bonds, etc.)

lives to 100

The employee has the choice of two contributions:

Scenario 1: $10,000 annual pre-tax contributions

Scenario 2: $7,600 annual after-tax contributions

The contributions are equivalent at the 24% tax rate.

Scenario 1: Pre-Tax Contributions

The employee receives an income tax deduction for their contributions. Their $10,000 contributions are invested at the start of each year and grow 7% annually.

By age 75, the employee’s portfolio grows to about $1.3 million.

However, they must take Required Minimum Distributions (RMDs) based on the Uniform Lifetime Table. The withdrawals count as taxable income and are taxed 24%.

The owner only use some of the money to pay taxes and invest the rest in investments which don’t earn income. These investments also earn 7% a year.

Over time, the pre-tax account shrinks and the brokerage account grows:

Age 80: $1.14 million pre-tax, $508,000 brokerage

Age 90: $553,000 pre-tax, $2.20 million brokerage

Age 100: $48,000 pre-tax, $5.07 million brokerage

The Required Minimum Distributions cause them to pay about $568,000 in federal taxes between age 75 and 100.

Scenario 2: After-Tax Contributions

With after-tax contributions, the employee receives no deduction for their contributions. The $7,600 they add each year grows 7% annually.

By the time they turn 75, the portfolio has grown to about $1 million.

However, they don’t have to take Required Minimum Distributions! Growth continues to compound.

The after-tax account grows with time.

Age 80: $1.41 million

Age 90: $2.78 million

Age 100: $5.46 million

They pay only $50,400 in federal taxes ($2,400 * 21 years) because they were taxed on the seed.

Tax Comparison

The pre-tax contributions (Scenario 1) would cost more than 10 times as much in federal lifetime taxes as the after-tax contributions (Scenario 2):

$568,000 for pre-tax contribution RMDs (fruit)

$50,400 for after-tax contributions (seed)

Total Portfolio Comparison

The total portfolio value is initially higher for the pre-tax contributions (Scenario 1) than the after-tax contributions (Scenario 2). They later flip.

Age 70: $944,000 pre-tax, $718,000 after-tax

Age 80: $1.65 million pre-tax, $1.41 million after-tax

Age 90: $2.76 million pre-tax, $2.78 million after-tax

Age 100: $5.12 million pre-tax, $5.46 million after-tax

After-Tax Comparison

At the end of age 74, the portfolios are identical on an after-tax basis:

$1.24 million pre-tax

$941,000 after-tax

$1.24 million less 24% in taxes equals the $941,000 after-tax (rounded).

The taxes on the Required Minimum Distributions causes the pre-tax contributions (Scenario 1) to fall behind on an after-tax basis.

Age 80: $1.38 million pre-tax, $1.41 million after-tax

Age 90: $2.62 million pre-tax, $2.78 million after-tax

Age 100: $5.11 million pre-tax, $5.46 million after-tax

Contribution Limits

The contribution limits are the same and linked for:

traditional (pre-tax) and

Roth (after-tax) contributions.

However, that may still result in larger effective contributions for Roth accounts.

There’s another after-tax option with much higher contribution limits.

Same for Traditional and Roth

How much can be contributed to an IRA, 401(k), 403(b), and 457(b) is usually the same for:

traditional (pre-tax) and

Roth (after-tax).

At the same limit, maxing the after-tax contribution has a bigger impact than maxing the pre-tax contribution. It’s like also contributing the taxes paid!

Combined for Traditional and Roth

The contribution limits of traditional and Roth are combined.

How much an 49 year old employee can contribute to a Roth 401(k) in 2024 is $23,000 less what they contribute to a traditional 401(k).

After-Tax

Some employers offer an after-tax plan which isn’t Roth. These plans have much higher limits and can be a way for employees who’ve maxed out their other options to save even more.

For 2024, the defined contribution limit is $69,000. That cap includes all contributions from both employer and employee.

Example

Jen contributes $23,000 to her 401(k)

Her company matches $10,000

Jen could contribute $36,000 to her After-Tax (not Roth) account

Future Income

The amount and consistency of income may also impact the decision to contribute to pre-tax or after-tax.

Income sources include:

deferred compensation

part-time, contract, or spousal income

Social Security or pension benefits

business profits

rental or royalty income

inheritance of a pre-tax retirement account…

After-Tax for High Future Income

Those expecting consistently high income may be ahead to make after-tax contributions.

In the future, their income will likely exceed their standard deduction and lower tax brackets. Taxable retirement income would likely be taxed at a high rate.

After-tax contributions could help them avoid even higher taxes.

Pre-Tax for Low Future Income

The opposite is true for lower future income.

If someone expects to earn very little sometime in the future, they might make pre-tax contributions to delay income until their tax rate falls.

Early Retirement

Lower income is especially common for early retirees who might have years or even decades between when:

they stop earning income and

start earning pension and/or Social Security benefits.

Launching a Business

Starting a new business can be like planting a garden:

the first year, it sleeps

the second year, it creeps

the third year, it leaps

The early years may offer opportunities to realize income by converting funds from pre-tax to after-tax. A Roth conversion is one example.

Pre-Tax for Variable Income

Some people choose to have inconsistent income. They work more when they need money and less when they don’t.

Also, some jobs, careers, and even industries have highly variable compensation.

Pre-tax contributions are well suited for inconsistent income.

They can:

lower income in high income years

raise income in low income years

quickly grow balances which may need to be used early in life

Spending Timeline

A 10% penalty usually applies if someone withdraws pre-tax retirement funds before age 59.5.

Pre-Tax Exceptions

Fortunately, there are exceptions to the penalty.

Depending on the account type, exceptions include:

birth or adoption,

education expenses,

separation from service after age 55,

substantially equal payments,

medical expenses,

disaster recovery,

disability,

divorce,

death…

However, not all of them are fun!

After-Tax

Contributions to an after-tax account can be withdrawn tax and penalty free. However, conversions and growth may be subject to income tax.

There are good reasons someone may need to withdraw funds before age 59.5:

paying down high-interest debt,

starting a business,

buying real estate, etc.

After-tax contributions provide more flexibility if the money’s needed early in life.

Future Tax Rates

Whether to make pre-tax or after-tax contributions could depend more on state than federal taxes.

Federal

Federal income taxes are primarily based on income and filing status.

I don’t attempt to predict future federal taxes, especially given the potential sunset of the Tax Cuts and Jobs Act.

Today’s federal tax system is likely as good a starting place as any. It’s progressive and has a high estate tax exclusion.

State

However, taxes vary from state to state.

Also, people move. Think of all the people who move to Florida in their later years - including my father!

Income Tax

If someone plans to move from a lower to a higher income tax state, it may make sense for them to contribute to an after-tax account now.

The opposite may be true if they plan to move to a state without income tax.

Estate Tax

Some states have exclusions much lower than the federal level.

Here in the Pacific Northwest:

Washington’s estate tax starts at $2.193 million

Oregon’s estate tax starts at just $1 million

The size of the estate generally doesn’t depend on whether it’s pre-tax or after-tax. After-tax contributions may lower estate taxes.

Lifespan

Pre-tax and after-tax accounts are treated very differently later in life.

Pre-Tax RMDs

An account holder considers a pre-tax account an asset. The U.S. government views it as untaxed income.

Uncle Sam wants his money! Required Minimum Distributions (RMDs) are how the federal government collects income taxes before end of life.

Each year, an account holder is required to withdraw a percentage of a pre-tax account based on their age. The percentage grows each year and is based on average life expectancies.

The age someone is required to start taking Required Minimum Distributions is changing:

however, it’s scheduled to rise to age 75 as part of the SECURE Act

No After-Tax RMDs

There are usually no Required Minimum Distributions (RMDs) for after-tax accounts. The federal government already taxed the seed and has no claim on the fruit.

Not having Required Minimum Distributions simplifies someone’s finances late in life. Simplicity can be especially important if someone suffers a health setback or cognitive decline.

After-Tax Longevity

Living longer extends the time funds can compound. Someone may enjoy decades of tax-free growth!

Marriage can also extend the timeline. A spouse who inherits a pre-tax retirement account can normally treat it as their own.

The IRS recognizes that reality and has a separate table to use for RMDs:

… if the sole beneficiary of your IRA is your spouse and your spouse is more than 10 years younger than you…

This longevity impact tends to favor after-tax contributions.

However, marriage also increases the standard deduction and raises the income tax brackets. That may result in paying lower rates on earned income, which makes pre-tax contributions more attractive.

As such, marriage has a mixed impact on the decision to make pre-tax or after-tax contributions.

Tax Diversification

For better or for worse, the future’s uncertain. It may make sense to keep a mix of pre-tax and after-tax accounts as a tax hedge.

Hey, thanks for reading my post on whether to contribute to a pre-tax or after-tax retirement account.

Just a reminder, I share a lot of resources that can help you.

Disclaimer

In addition to the usual disclaimers, neither this post nor these images include any financial, tax, or legal advice.