Will You Owe Estate Tax?

Hello, I’m Kevin - a financial planner who helps tech professionals and their families live great lives.

Make yourself at home - we’ll get to estate and inheritance taxes in a moment.

But first - here are some links you may want to save for later.

How to Minimize Lifetime Taxes

Contribute to Pre-Tax or After-Tax?

Now, let's get on to the blog! 😀

Good Question

A recent conversation inspired today’s article.

I was speaking with someone who’s:

single,

lives here in Washington state, and

has a net worth of about $5 million.

He had no idea that Washington has a state estate tax or that he’s already subject to it!

Based on his net worth projection, his estate may have to pay over $2 million in Washington estate tax!

What Is Estate Tax?

Estate tax is a tax someone pays after death.

It’s basically a tax on those who - in the eyes of state and federal government - accumulated too much wealth by the end of their lives.

Technically, no-one pays an estate tax. They’re dead!

However, their estate might.

Fortunately, there are exemptions! Unfortunately, those exemptions are subject to change and vary wildly by state.

Federal Estate Tax

The estate tax in the news is the federal one.

Current Exemption

For 2024, the federal estate tax exemption is $13.61 million.

That’s pretty high - especially considering married couples can double it with something called DSUEA:

Deceased

Spouse

Unused

Exemption

Amount

This allows a married couple to combine their exemptions to $27.22 million if certain conditions are met.

How We Got Here

Previously, the federal estate tax exemption was much lower and taxed at a higher rate.

Rose Over Time

The exemption grew over 5x quickly:

from $650,000 in 1999

to $3.5 million in 2009

The highest estate tax rate also fell 10%:

from 55% in 1999

to 45% in 2009

Increased to $5 Million Plus Inflation

New legislation created in 2009 and 2010 raised the exemption to $5 million.

George Steinbrenner - the owner of the New York Yankees - died as the federal estate tax was changing. His approximately $1.1 billion estate paid no federal estate tax because he passed in 2010!

Legislation adjusted the federal exemption to $5 million plus inflation after 2011.

The top-end estate tax rate trended down. It:

fell from 45% in 2009

to 35% in 2010, and then

grew to 40% in 2013 - where it is today.

More Than Doubled the Exemption

The Tax Cuts and Jobs Act of 2017 raised the exemption to $11.18 million, indexed for inflation. It’s grown to $13.61 million as of 2024.

Scheduled to Drop

However, the higher exemption only goes through the end of 2025. It’s scheduled to fall back to $5 million plus inflation since 2011 on Jan. 1, 2026.

Unified Gift and Estate Tax

The federal estate and gift tax system is combined. Taxable gifts eat into the lifetime exemption.

Gifts above $18,000 are generally taxable in 2024.

A married couple can double that exclusion amount by gift splitting. Together, they could give $36,000 a year to an individual before it starts to reduce either of their $13.61 million lifetime exemptions.

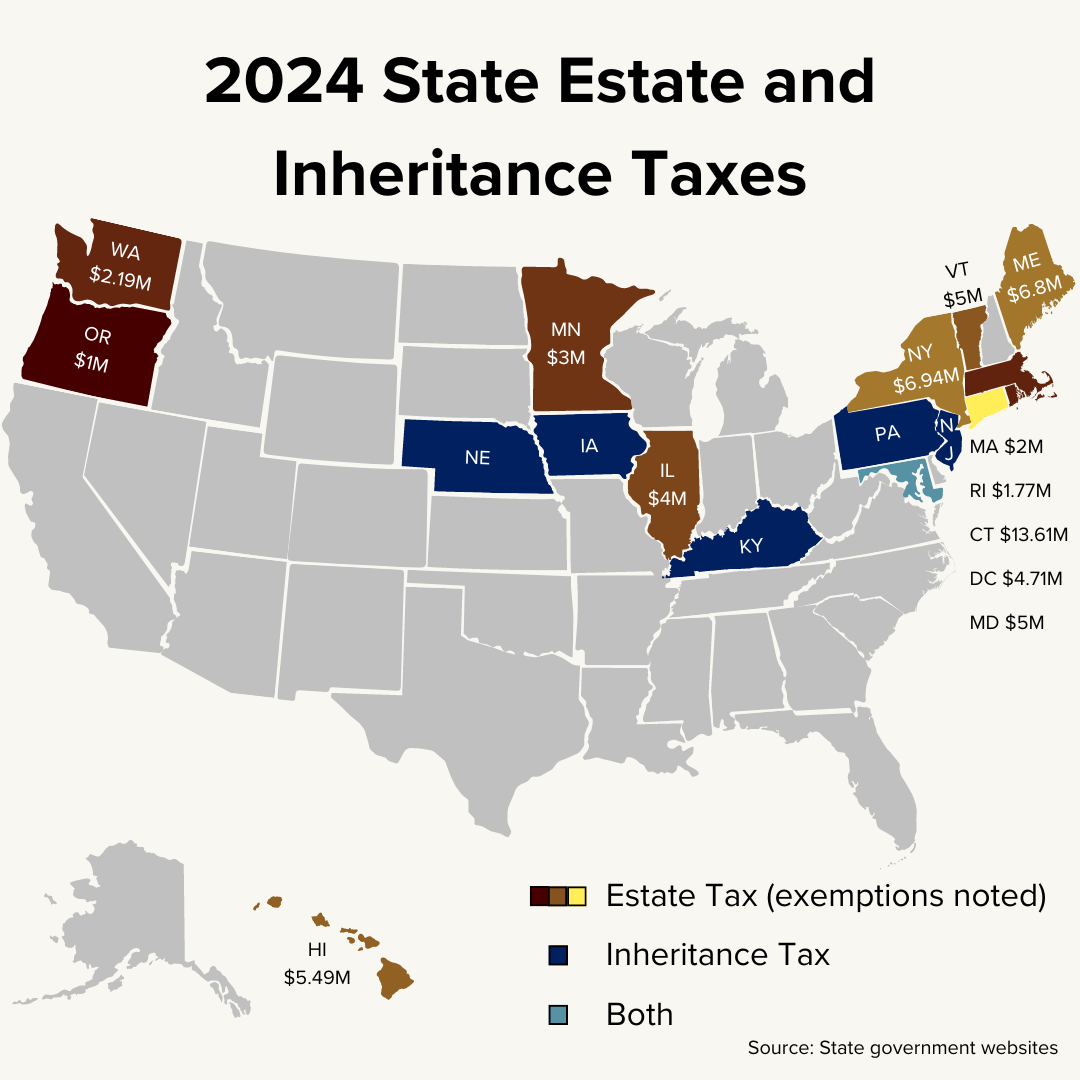

State Estate and/or Inheritance Tax

18 states have an estate tax, inheritance tax, or both.

States with an Estate Tax

13 states have an estate tax which are on top of the federal estate tax. Each state exempts or excludes a portion of estates from taxes.

However, only one state - Connecticut - follows the federal limit. The other states’ exemptions are lower, causing more people to be taxed.

Below is each state’s (rounded) estate tax exemption or exclusion:

States with an Inheritance Tax

Six states have an inheritance tax. Maryland has both an estate and inheritance tax.

Here’s how state inheritance taxes generally work:

beneficiaries pay the tax

only be a few thousand dollars may be excluded

tax rates depend on how closely related the beneficiary was to the deceased

the closer the relation, the lower the tax rate

The six states with an inheritance tax are:

How Much Could It Cost?

The cost of estate and inheritance taxes can be huge!

Here in Washington state, the highest estate tax rates are:

40% federal plus

20% state

That means at least a portion of someone’s estate could be taxed 60%!

How to Reduce Estate Taxes

There are many ways to reduce estate taxes. Some of them are more fun that others!

Spend It

This may be the most fun!

Maximizing Spending

Some questions I might ask myself in that situation include:

Are my long-term care costs fully funded? (Nope.)

Is my house paid off? (It’s not.)

Are there any updates I’d like to do to my home? (Several.)

Do I need to buy a new car? (Yes, ours is a decade old.)

Are there any trips I’d like to take? (Oh, yeah!)

What have I not done that I’d like to do in life? (Wait - that’s personal!)

Conducting Tests

For someone who’ll likely be subject to the federal estate tax, it may make sense to test spending more.

I like to think of every expense as a hypothesis.

My hypothesis is this expense will positively impact my life.

I test is by making the purchase.

Did the expense improve my life?

If so, I might repeat or even expand it.

If not, I’ll probably cut it.

Either way, I learn something!

Enjoy It Now

Aging takes its toll:

senses dull,

bodies weaken, and

energy fades.

The same dinner in Paris literally may not look, smell, and taste the same in 30 years.

I recently saw a tragic photo of an older couple fast asleep on a gondola ride in Venice. The fellow navigating the boat looked to a fellow gondolier with an expression of:

Now, what?

The couple may have waited too long to take that trip!

Who, Not What

At some level of wealth, spending becomes more about who than what.

Who’s invited to that:

nice dinner?

weekend trip?

European vacation?

Doing those things while everyone still has their health can create once in a lifetime experience.

Get or Stay Married

Making major life decisions for money is cringeworthy. It’s even worse with romance!

Nonetheless, the Deceased Spouse Unused Exemption Amount (DSUEA) effectively doubles the estate tax exemption.

If both spouses are U.S. citizens, they can usually gift each other as much as they like without having to worry about limits or gift tax. That opens up some other planning opportunities.

Donate It

Charitable contributions can lower estate and/or inheritance taxes. Someone must be able to afford giving to consider it.

Giving assets away to qualify for Medicaid is generally a bad idea!

The U.S. government is wise to that scheme and sifts through previous transactions for any gifts or donations. Amounts given within the last five years would delay Medicaid benefits and require medical expenses be paid out of pocket!

That could be nearly impossible if someone would otherwise qualify for Medicaid.

Contribute to a Donor Advised Fund

A Donor Advised Fund (DAF) is an interesting tool.

Benefits of a DAF

These funds can:

receive contributions - and hopefully a tax deduction - now,

grow through investing, and

be distributed to qualifying charitable organizations later.

They’re also fairly easy to set up and fund.

Someone can even contribute highly appreciated assets! Doing so avoids the capital gains they’d have to pay if they sold them.

Nonprofits don’t mind selling them for a gain because they don’t pay income taxes! Donor Advised Funds often sell single stocks right away to diversify contributions.

Contributing to a DAF can be especially helpful in years with abnormally high income.

Income tax is progressive. Funding a Donor Advised Fund can lower income for higher than usual tax rates.

Drawbacks of a Donor Advised Fund

However, a DAF is not always the best option!

For instance:

Charitable contributions work best if someone already itemizes expenses for their tax return. Otherwise, someone would need to give more before it lowers their taxes.

It would generally be better to sell investments which have fallen in value to get the tax benefit nonprofits can’t.

Holding appreciated assets until death could make sense because those assets receive a step-up in basis. That could result in less tax for heirs.

There are many other planning techniques which may be more appropriate, depending on the situation.

Give to Individuals Now

Another option is to start giving to individuals.

Exemptions and Exclusions

This is where that $18,000 per person or $36,000 per couple gift tax exclusion can come in handy. Annual gifts to to many family members can move significant wealth to future generations.

Larger gifts may also avoid gift tax such as:

tuition paid directly to an educational institution or

medical expenses paid directly to healthcare institutions.

Benefits of Giving While Alive

It could make sense to give with a warm hand instead of a cold one. The giver gets to see recipients enjoy it!

Also, gifts now might make a material impact on someone’s life. They might not need it by the time the donor passes!

Giving while still alive offers the opportunity to teach the recipient:

about the gift,

investing tips, and/or

life lessons.

It’s also helpful to learn how the recipient responds:

How do they spend it?

Did they appreciate it?

Was it a burden?

Did it impact their relationship with the giver?

Giving a little can help someone learn a lot! It’s especially helpful to do so when someone has all their cognitive abilities.

Giving now also allows the assets less time to grow. Avoiding growth can further reduce estate and/or inheritance taxes.

Give to Individuals Now

Someone may also choose to give at the end of their life.

Benefits of Bequeathing

Giving at death is especially helpful if someone with means wants to remain anonymous. Flashing cash can bring unwanted attention!

End of life giving can also significantly reduce the risk of running out of money. A long stay in a nursing or hospice facility is unlikely. However, a decade stay might cost hundreds of thousands or even millions of dollars!

End of life giving also gives assets more time to grow.

At a 7% annual return, $10 million might become:

$20 million in 10 years

$39 million in 20 years

$76 million in 30 years

Drawbacks to Bequeathing

It’s crucial to plan carefully for end of life giving.

Estate plans get stale over time:

people move to a new state,

divorces and re-marriages occur,

children or grandchildren are born…

Title and beneficiary designations are extremely important. They pass by law automatically - not based on what’s in someone’s Last Will & Testament!

Assets can get misplaced - especially if only one person knows about them! Looking at you, crypto.

Wills can be contested, which can get ugly. At death can tear a family apart.

Planning and communication are key to avoiding a mess. I consider estate planning as the ultimate act of love.

Hey, thanks for reading my post on estate taxes.

Just a reminder, I share a lot of resources that can help you.

Disclaimer

In addition to the usual disclaimers, neither this post nor these images include any financial, tax, or legal advice.

Estate planning is an entire branch of financial planning. This article barely scratched the surface of opportunities.

Because I work with clients from coast to coast, I’m interested in all the state estate and inheritance taxes. However, I’m neither an accountant nor an attorney.

Estate and inheritance tax is one of the most active areas of tax legislation. This article may be out of date as soon as it’s published.

Finally, the data is state specific and not easy to locate. I’ve done my best to research, cite, and link the latest rules.