Potential Financial Steps for Tech Professionals in March

Hello, I’m Kevin - a financial planner who helps tech professionals and their families live great lives.

Make yourself at home - we’ll get to potential steps for March in a moment.

But first - here are some links you may want to save for later.

Are Employee Stock Purchase Plans Underrated?

Now, let's get on to the blog! 😀

Growing season

This weekend was beautiful here in the Pacific Northwest.

Power outages were the biggest challenge for our area this winter. Our generator got a workout!

The days are getting longer, leaves are budding, plants are sprouting… spring has sprung!

Potential steps for tech professionals this month

Financial steps for March include:

Select employee stock contribution %

Plan major purchases

Finalize last year contributions

Prepare taxes

Schedule summer Paid Time Off (PTO)

1. Select employee stock contribution %

Some companies offer an Employee Stock Purchase Plan (ESPP) with a:

15% discount and a

six-month lookback.

That plan takes 15% off the lower price at the beginning and end of each six month period.

Example:

Mike works for a tech company and maxes his ESPP with 15% of his gross income each paycheck.

At the end of six months, his employer uses the funds to buy stock at a discount. If Mike leaves the company before the purchase, he’ll receive the cash instead.

What happens if the stock price rises from $100 to $110?

Mike would buy at $85, 15% off $100.

However, the stock’s worth $110!

That's a 29% gain ($25 / $85).

What happens if the stock price falls from $100 to $90?

Mike would buy at $76.50, 15% off $90.

However, the stock’s worth $90!

That’s an 18% gain ($13.50 / $76.50).

If able to sell right away, Mike might only hold the shares a day or two.

Participating in the Employee Stock Purchase Plan may offer higher returns and lower risk than holding company shares.

Maximum ESPP contribution

The maximum qualified Employee Stock Purchase Plan contribution each year is:

15% of compensation, up to

$25,000 a year.

Compensation includes salaries, wages, bonuses, and commissions. It doesn’t include Restricted Stock Unit vests.

Not for everyone

However, participating in an ESPP isn’t for everyone.

It may not make sense for households with:

high interest debt,

living expenses higher than income, or

large upcoming purchases.

For more, check out:

Are Employee Stock Purchase Plans Underrated?

Own Stock or Contribute to ESPP?

2. Plan major purchases

Now is a good time to prepare for big-ticket expenses.

Remodel

Home upgrades are often easier in the summer than in the winter. It’s much easier to move earth once it thaws! Also, planting in spring gives plants more time to grow before winter.

Buy a car

The least expensive time of the year to buy a car may be the fall. That’s when new models come out - which can result in good deals.

Someone may be able to minimize their costs by preparing now:

review their credit report,

pay down high balances,

update income (if it’s grown) with financial institutions…

Also, shopping around may save thousands on a car purchase. For more, check out: Buying a Car

Move

While it may be more expensive to buy a home in the summer, it’s easier to move. There’re also more homes on the market.

Families often prefer to move during the summer because it’s easier on children. Changing schools is hard enough without doing so during the school year!

3. Finalize last year contributions

There’s still time to make contributions for 2024!

Traditional IRA

Contributions to an Individual Retirement Arrangement (IRA) can be made up to April 15th, 2025.

It’s possible a family may earn too much to either:

receive a tax deduction on a pre-tax (traditional) IRA or

be able to contribute directly to a Roth IRA.

Roth IRA

A Roth IRA works differently. There’s no tax deduction for the contribution on the front end. Contributions are taxed initially.

However, they may never be taxed again if certain conditions are met!

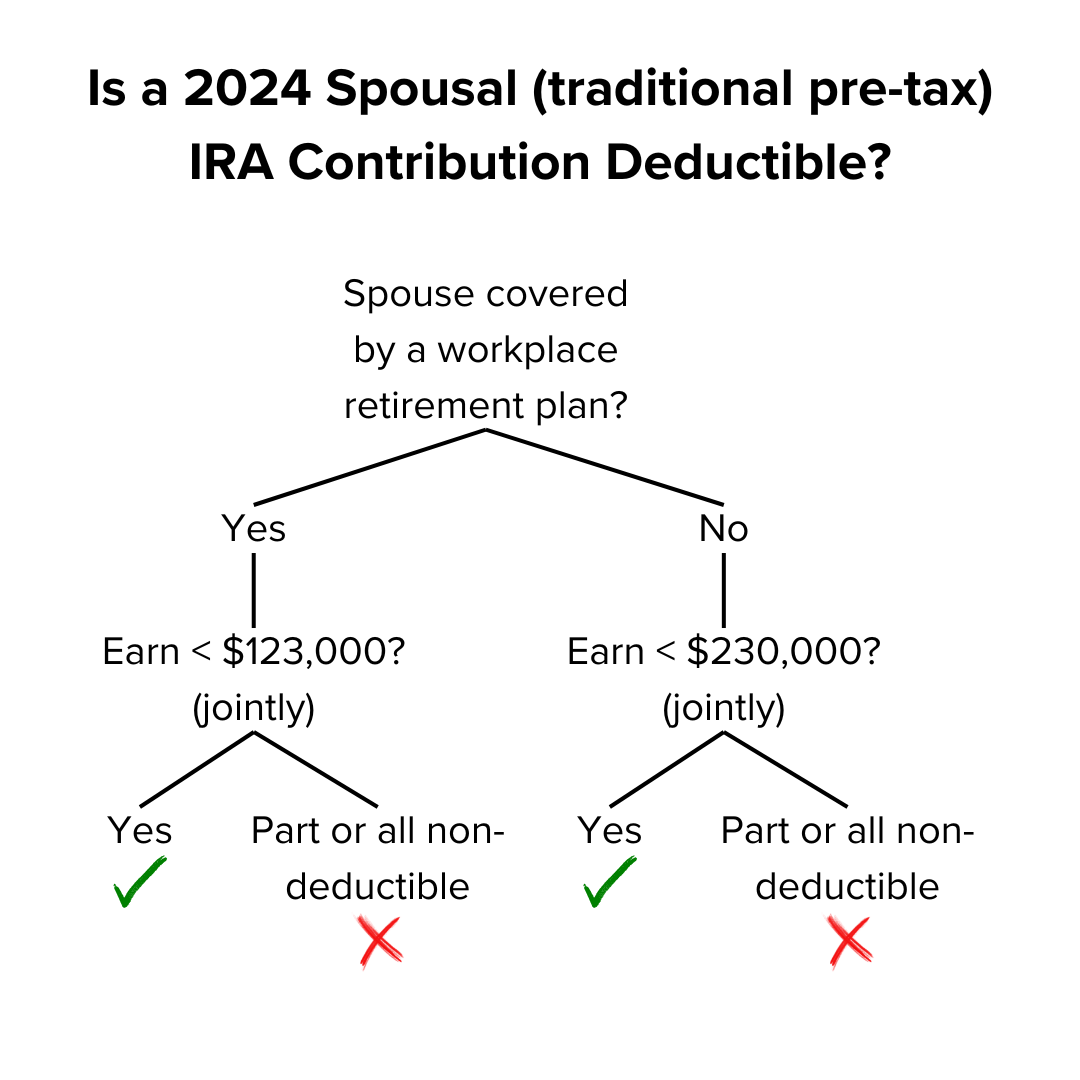

Spousal IRA

A spouse without earned income might still be able to contribute to a traditional or Roth IRA!

The couple would need to earn enough to fund all their retirement contributions. This is known as a spousal IRA.

Whether pre-tax contributions would lower taxable income depends on:

whether the spouse was covered by a retirement plan at work and

how much the couple earned in 2024.

Here’s a quick decision tree with the income limits:

Health Savings Account

If someone was on a qualifying High Deductible Health Plan (HDHP) by December 1st, 2024, they have until April 15th, 2025 to contribute to a Health Savings Account for last year.

The primary benefit of an HSA is that contributions are triple tax advantaged. They:

lower taxable income when made,

grow tax-free, and

can be used tax-free for qualified medical expenses.

According to the IRS, the 2024 contribution limits are:

$4,150 for individual coverage and

$8,300 for family coverage.

For more, check out:

Pros and Cons of a Health Savings Account

4. Prepare taxes

Even if taxes are self-prepared, it’s important to dedicate time to them.

Scheduling time is even more important when working with a tax professional! They’re overworked and in high demand.

Get organized and come prepared.

Tax checklist

Everyone’s busy. Things get missed - even by tax preparers!

Crashes happened frequently in the early days of aviation. Using checklists significantly improved safety.

Checklists have expanded to other areas like:

building construction,

truck driving, and

surgery.

We even use checklists when getting ready to sail!

One thing I like to do both for myself and for clients is draft a tax checklist. It lists everything I know that could impact taxes for the year!

A good place to start is the previous year’s tax documents:

Which still apply?

Are there any changes?

Creating the checklist also reminds me of other tax items!

5. Schedule summer Paid Time Off (PTO)

Now’s a wonderful time to book Paid Time Off (PTO) for the summer!

Vacation rentals begin to book.

Flight prices start to rise.

Calendars get full.

Call Dibs

It’s not just the calendars of your friends and family members. You also have to worry about your coworkers’!

Summer coverage can be a struggle for many teams. People who schedule late may have limited say in which days they can take off. 😯

Claim the days which work best for you and your family now!

Use It or Lose It

Many companies limit how many hours can be rolled over from year to year. Hours above the limit are involuntarily donated to the company.

Full time employees can often roll over two weeks (80 hours) at the end of the year. However, it can vary.

During my tenure with T-Mobile, the rollover:

shrank to as little as 1 week (40 hours) and

grew to as much as 3 weeks (120 hours).

Avoid the drama. 🎭 Schedule Paid Time Off (PTO) now!

Hey, thanks for reading my post on potential steps tech professionals can take in March.

Just a reminder, I share a lot of resources that can help you.

Disclaimer

In addition to the usual disclaimers, neither this post nor these images include any financial, tax, insurance, or legal advice.