How to Use Credit Reports to Improve Credit Scores

Hello, I’m Kevin - a financial planner who helps tech professionals and their families live great lives.

Make yourself at home - we'll get to potential steps for July in a moment.

But first - here are some links you may want to save for later.

Get a HELOC Before Retirement?

Are You Less Behind Than You Think?

Now, let's get on to the blog! 😀

What Are Credit Scores?

According to the Consumer Financial Protection Bureau:

A credit score is a prediction of your credit behavior, such as how likely you are to pay a loan back, based on information on your credit reports.

Companies use credit scores to make decisions on whether to offer you a mortgage, credit card, auto loan, and other credit products, as well as for tenant screening and insurance.

They are also used to determine the interest rate and credit limit you receive.

Most credit scores range from 300-850.

Credit Scores Matter!

Credit is tricky:

Those who need it have trouble getting it.

Those who can get it often don’t need it.

Six Credit Categories

The Consumer Financial Protection Bureau (CFPB) categorizes credit as:

Superprime (800 plus)

Prime plus (720 to 799)

Prime (660 to 719)

Near-prime (620 to 659)

Subprime (580 to 619)

Deep subprime (579 or less)

The data in this article are for what the CFPB calls “general purpose” credit cards:

… those that transact over a network accepted by a wide variety of merchants…”

Those are not retailer-specific, or charge, cards.

Cost of Debt

The average total cost of credit card debt for superprime borrowers was about a third that of deep subprime borrowers in 2023:

12% for superprime

36% for deep subprime

About two-thirds of that expense was interest. The remaining third came from fees.

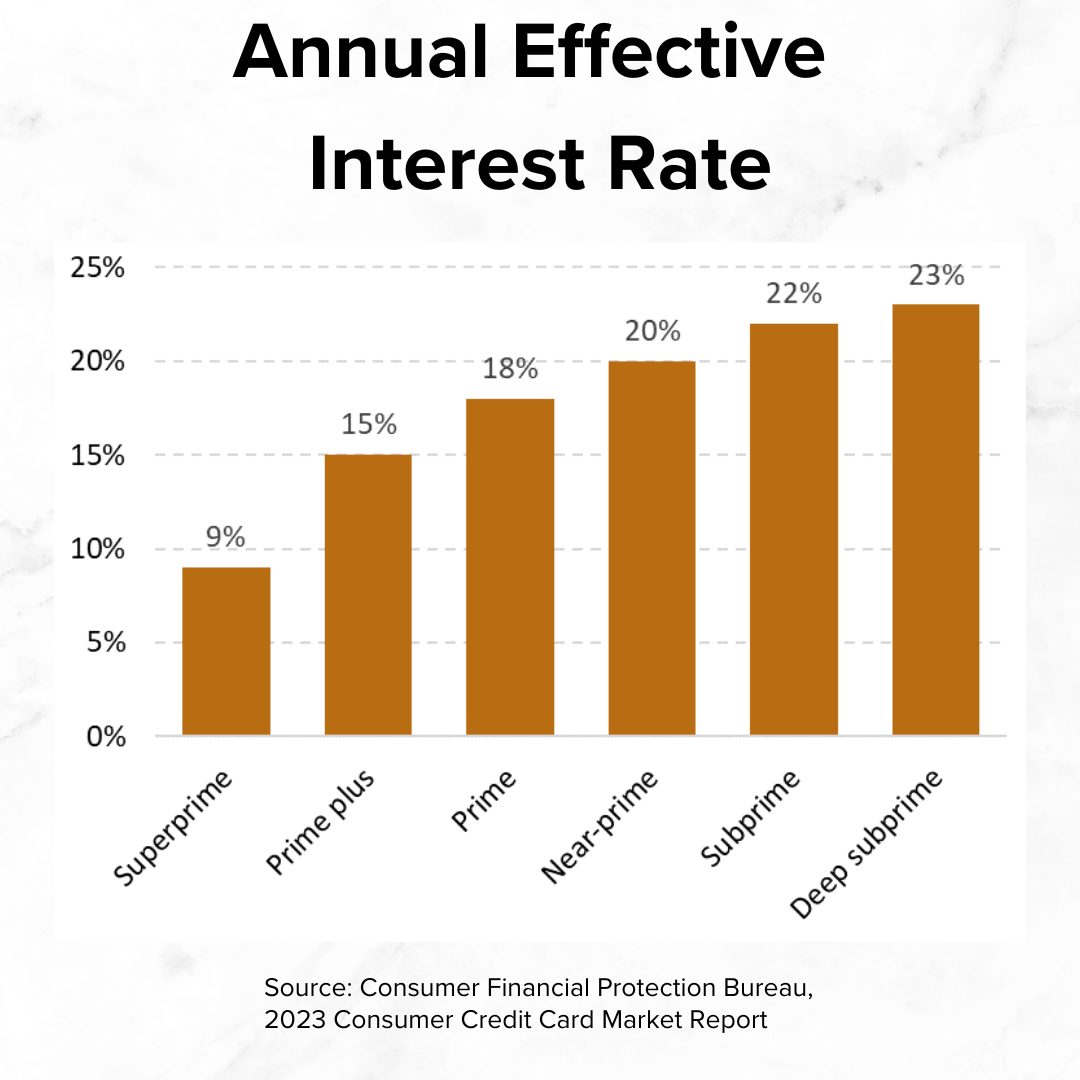

The annual effective interest rates by credit tier was:

Superprime 9%

Prime plus 15%

Prime 18%

Near-prime 20%

Subprime 22%

Deep subprime 23%

Borrowers with a prime credit rating are less likely to pay:

late fees,

debt suspension fees,

returned payment fees, etc.

Credit Approval

The approval rate for superprime borrowers was about five times that of subprime and deep subprime borrowers:

Superprime 86%

Prime plus 79%

Prime 63%

Near-prime 41%

Subprime and deep subprime 17%

Superprime borrowers also received a credit limit about 12 times that of deep subprime borrowers.

Unfortunately, subprime and deep subprime borrowers are also:

more likely to forfeit their credit card rewards and

less likely to receive credit on disputed charges.

How Are Credit Scores Calculated?

Also according to the Consumer Financial Protection Bureau:

Companies use a mathematical formula - called a scoring model - to create your credit score from the information in your credit report.

One of the most popular is the FICO® Score.

(FICO stands for the Fair isaac Corporation.)

Credit Score Factors

The consumer division of the company, myFICO, states the credit score is based on:

payment history (35%)

amount owed (30%)

length of credit history (15%)

new credit (10%)

credit mix (10%)

Payment History (35%)

The biggest drive of the credit score is payment history. Often, the best predictor of future behavior is past behavior.

In its educational video, myFICO highlights missed payments. If missed:

How often?

How recently?

How late were they?

Major Items

Of bigger concern are items like:

debts turned over to a collection agency,

foreclosures, and

bankruptcy.

These are more serious and significantly lower credit scores.

The impact depends on the recency, frequency, and severity.

Bankruptcies remain on a credit report for 7-10 years, depending on the type. Collections stay on the credit report for seven years.

For more, check out Payment History on myFICO.

Correct Payment History

There’s not much that can be done about accurate payment history. However, there may be either missing or false information.

Dispute Inaccuracies

Since derogatory items have the biggest impact, start there. Check them for accuracy. There’s always a chance of human error!

If needed, reach out to the reporting financial institution directly for more information.

Dispute any inaccurate information with all three of the major credit bureaus:

TransUnion, and

Attack Fraud

There can be outright fraud on an account. Reviewing a credit report can help catch it!

In the case of fraud, the first step is to contact the financial institution. It may also make sense to freeze credit to avoid further misuse. Then, dispute the charges. It can take several disputes over years to fully clear fraud from credit reports.

Resolve Issues

Autopay may have fallen off for a credit card. An authorized user or co-signer may be using credit inappropriately.

Correcting issues as soon as possible can prevent further headache.

Amount Owed (30%)

Having an account balance near a credit limit is concerning to lenders.

Growing interest charges make debt difficult to pay down. There’s also less financial flexibility.

Utilization

Utilization is the percentage of credit used:

outstanding balance / credit limit

It matters both for each account and overall. Lower is generally better.

Snapshot

Unlike payment history, the amount owed on each account is a snapshot.

A large recent purchase or a payment which hasn’t cleared could lower credit scores.

For more, check out Amount of Debt on myFICO.

Lower Utilization

The amount owed matters less than the utilization. Someone with a large balance and a huge credit limit may have a good credit score.

Balance Accounts

Also, 10 accounts with 10% utilization each is perceived as less risky than one account with 100% utilization.

Consider:

spending a little more on unused credit cards and

paying down larger balance

Doing so helps:

spread utilization across multiple cards

ensure each card remains open!

Credit companies primarily make money from:

interest,

fees, and

merchant transactions.

If someone pays off their credit card each month, the company’s unlikely to receive any interest or fees. Howedver, they could still receive the merchant transaction revenue.

Credit that isn’t used is unprofitable for the lender. They’ll cancel the credit, which:

reduces the overall credit limit,

raises the utilization, and

lowers someone’s credit score.

Pay Down Balances

Another opportunity is to pay down balances. This is especially important before financing a major purchase like an appliance, vehicle, or home.

The snapshot could work to someone’s advantage. Making payments in the short-term can help improve a credit scores and lending terms.

However, it’s important to start several months in advance. It takes time for changes to reflect on credit reports.

Raise Credit Limits

A third way to lower utilization is to increase credit limits.

Update Income

Income trends up until at least middle age. However, financial institutions don’t know unless consumers tell them!

Update income information after big raises or promotions. Include all applicable income for everyone in the household if that’s allowed.

Income can come from many source - not just base salaries and wages!

commissions and bonuses,

rent and royalties,

Social Security and pensions,

investment income, etc.

Anything included on a tax return might count.

Reporting higher income may automatically raise credit limits.

Request Credit LImit Increases

A more direct way to increase a credit limit is to ask.

Many companies offer the option to “request a credit limit increase” when logged into the account. It’s possible doing so will be approved with a soft inquiry.

If not, it may make sense to strategically request a credit limit increase with a hard inquiry. If possible, only do one or two hard inquires a year - including new credit applications.

There are downsides - including:

more credit is tempting to use,

higher credit limits come with more fraud risk, and

hard inquiries may temporarily lower credit scores.

Length of Credit History (15%)

Someone with a long history of responsible credit is less risk than someone without established credit.

Age of Account

According to myFICO, this factor is based on the:

oldest,

newest, and

average account age.

Context

Length of credit history provides context for the other credit data.

Let’s say two people missed a payment:

one has been responsible with their credit for 20 years

the other just got credit last month

The missed payment is much more concerning for the unproven creditor.

For more, check out Length of Credit History on myFICO.

Lengthen Credit History

It may seem like little can be done for the credit history timeline. However, there are some ways to lengthen it.

Keep Older Accounts

It often makes sense to keep the oldest credit card accounts active. Use them at least once a month - even if they’re immediately paid off.

Keeping older accounts grows both the:

age of the oldest account and

average account age.

Doing so may be even more important as someone pays off:

car loans,

student loans, and

mortgages.

An installment loan like these may be someone’s oldest account. Paying it off if cause for celebration!

Bizarrely, paying it off could lower someone’s credit score.

Close Newer Accounts

Another option is to close the most recently opened account. Doing so can be especially helpful if the card offered a temporary low introductory rate or cash bonus.

Eliminating the newest debt raises both the:

age of the newest account and

average account age.

However, doing so also:

lowers the overall credit limit,

increases utilization, and

could lower credit scores.

Pay Regular Installments

Car loans, student loans, and mortgages could last years or even decades.

Installment loans are often some of the lowest interest debt someone has. That’s especially the case for those who took out fixed, long-term loans a few years ago.

In addition, they’re often:

the largest debt balances someone has and

tax deductible.

Keeping them may:

minimize interest expense and

grow the average account age.

New Credit (10%)

Reasons somoene might apply for credit several times in a short timespan include:

rate shopping,

a need for more credit, or

denied applications.

The last two are especially concerning for creditors.

Hard Inquiry

When a borrower applies for credit, the creditor checks their credit. That check is reported as a hard inquiry on their credit report.

According to myFICO, a hard inquiry:

typically lowers your credit score and remains on your credit report for two years.

Unfortunately, this practice causes opposing cycles:

those approved may receive the credit limit they need and stop applying - which raises their credit scores

those denied need to continue to apply - which lowers their credit scores

Soft Inquiry

According to myFICO:

Rate shopping is accomodated for, and promotional, insurance and employment inquiries don’t count against you.

Credit checks not caused by applying for new credit are called soft inquiries.

Limit New Credit Applications

Instead of applying for new credit, it may make sense to leverage techniques already mentioned.

Keep Existing Accounts

Even if an older account is less than ideal, it may make sense to use it regularly. Using it could help keep it open.

Raise Credit Limits

As mentioned above, two ways to increase credit limits are to:

update income information with raises and promotions

request credit limit increases if they don’t result in a hard inquiry

Be Selective

A third option is to occasionally apply for new credit. Reviewing credit annually could remind someone to take out new credit sparingly.

A credit inquiry or two a year is unlikely to significantly effect credit scores. The credit limit increase and financial flexibility might be more beneficial than the slight dip.

Credit Mix (10%)

Creditors assess the risk of lending money through a variety of factors, one of them being your ability to successfully manage different types of credit.

Installment Accounts

An installment account usually requires a fixed payment each month until the balace is completely paid.

Examples include:

mortgage

auto loan

student loan

Revolving Accounts

A revolving account has more flexibility on how much is paid each month.

Examples include:

credit card

retailer card

gas station card

Home Equity Line of Credit (HELOC)

Improve Credit Mix

A credit report can highlight how to improve the mix:

if it’s all revolving debt, it may make sense to next apply for installment debt

the opposite might be true if it’s currently all installment debt

Own vs. Rent

Getting an installment loan is a potential benefit of owning a home or car instead of renting or leasing.

Some services work to include good payment history for recurring expenses like rent and utilities. However, those payments often are not not automatically included on a credit report.

Credit Cards

Credit cards:

are more widely accepted than either retailer or gas station cards,

tend to offer more cash back or points than debit cards, and

provide slightly higher fraud protection than other payment forms.

If there’s fraud on the account, the money spent is the financial institution’s. For many other payment types, the money spent is the account owner’s.

HELOC

A Home Equity Line Of Credit (HELOC) can be helpful for those who:

are planning a major remodel,

have paid off their mortgage, or

are retiring soon.

There may be tax benefits if all the funds withdrawn are used to improve a home. A HELOC is also a quick way to tap into home equity for living expenses.

Have Both

The key is to ensure someone has both types of credit accounts:

revolving

installment

How to Get a Free Credit Report

Each American can get a free credit report from the three major credit bureaus at least once a year.

Check out AnnualCreditReport.com for more detail.

Hey, thanks for reading my post on how to use credit reports to improve credit score.

Just a reminder, I share a lot of resources that can help you.

Disclaimer

In addition to the usual disclaimers, neither this post nor these images include any financial, tax, or legal advice.