How Does an ESPP Work?

By Kevin Estes

What Is an Employee Stock Purchase Plan?

An Employee Stock Purchase Plan (ESPP) offers employees the opportunity to buy company shares at a discount. That discount often depends on how the company stock does.

ESPPs are common for large tech companies. They’re usually qualified plans under section 423(c) of the federal tax code.

Non-qualified plans are less common yet do exist. This article focuses on qualified ESPPs.

How Much Is the Discount?

The maximum discount for a qualifying Employee Stock Purchase Plan is 15%.

Some companies offer less. However, the discount may also depend on whether the plan has a lookback.

Lookback Feature

An ESPP could take the lower of the price at the beginning and end of an offering period. The company “looks back” at the starting price to set the purchase price.

Say a plan offers a 15% discount and a six month lookback.

The price of the stock was:

$100 on 4/1 and

$110 on 9/30.

An employee participating in the program would buy at the lower of $100 and $110 - so $100.

The discount is then applied. The purchase price would be $85:

$100 less 15%

The lookback feature is like an option. That’s how the IRS refers to it!

It’s like employees are granted an option to buy the stock at 15% off the current price in the future.

The Best Plans

The most attractive Employee Stock Purchase Plans offer:

the maximum 15% discount,

a lookback feature, and

a long offering period.

A longer period gives the stock more time to grow before it’s purchased. With a lookback, the more a stock grows, the bigger the discount gets.

Extreme Example:

Say the stock doubles from $100 to $200 during the offering period. With a 15% discount, employees would purchase shares at $85.

That’s a gain of $115 on an $85 investment - a 135% gain!

How Much Can Be Contributed?

Up to 15% of gross income can be contributed to a qualified Employee Stock Purchase Plan.

For this definition, gross income includes compensation like:

salaries

wages

bonuses

commissions

However, it excludes vesting Restricted Stock Units.

There’s also an annual contribution limit of $25,000. A higher income employee might not be able to contribute a full 15%.

How Long Is the Offering Period?

The time between the offering date and the purchase date is known as the offering period:

offering date = date an employee can start contributing

purchase date = date shares are bought with the money the employee has contributed

Let’s say the company plan has a six-month offering period and the next one starts on 4/1:

offering date = 4/1

purchase date = 9/30

The offering period is 4/1 through 9/30.

Although it can be shorter or longer, ESPP offering periods are often six months.

Length is a bit of a mixed bag:

Shorter periods are easier on cash flow and make it easier for employees to participate.

Longer periods give the stock more time to grow before purchase.

How Can Someone Sign Up?

Employees can usually sign up to contribute to the Employee Stock Purchase Plan the month before the offering date.

If an offering period starts 4/1, the window to update the contribution percentage might open in early March.

The most common way to sign up is to increase the contribution percentage with the plan custodian (Fidelity, Vanguard, etc.) The default is no contribution (0%) yet can be set as high as 15% for a qualified ESPP.

How Are Purchases Made?

The amount an employee contributes to the ESPP each paycheck depends on:

how much they chose to contribute and

their gross income.

Gross income is before taxes and other deductions. Contributing 15% could lower their take-home pay much more!

After-Tax Contributions

Contributions are made after tax. They’re deposited to the ESPP instead of the employee’s checking account.

Purchase

The funds in the account at the end of the offering period are used to buy discounted shares of company stock.

The plan usually buys the most whole shares possible based on:

the account balance and

the purchase price.

Leftover funds are rolled over to the next offering period.

Example:

Jon earns a $100,000 base salary and is paid biweekly. Each paycheck, he grosses $3,846.15 ($100,000 / 26 pay periods).

His company offers a 15% discount with a six-month lookback.

Jon decided in early March to fully participate by contributing 15% of his salary to the Employee Stock Purchase Plan.

That period’s:

offering date was 4/1 and

the purchase was made on 9/30.

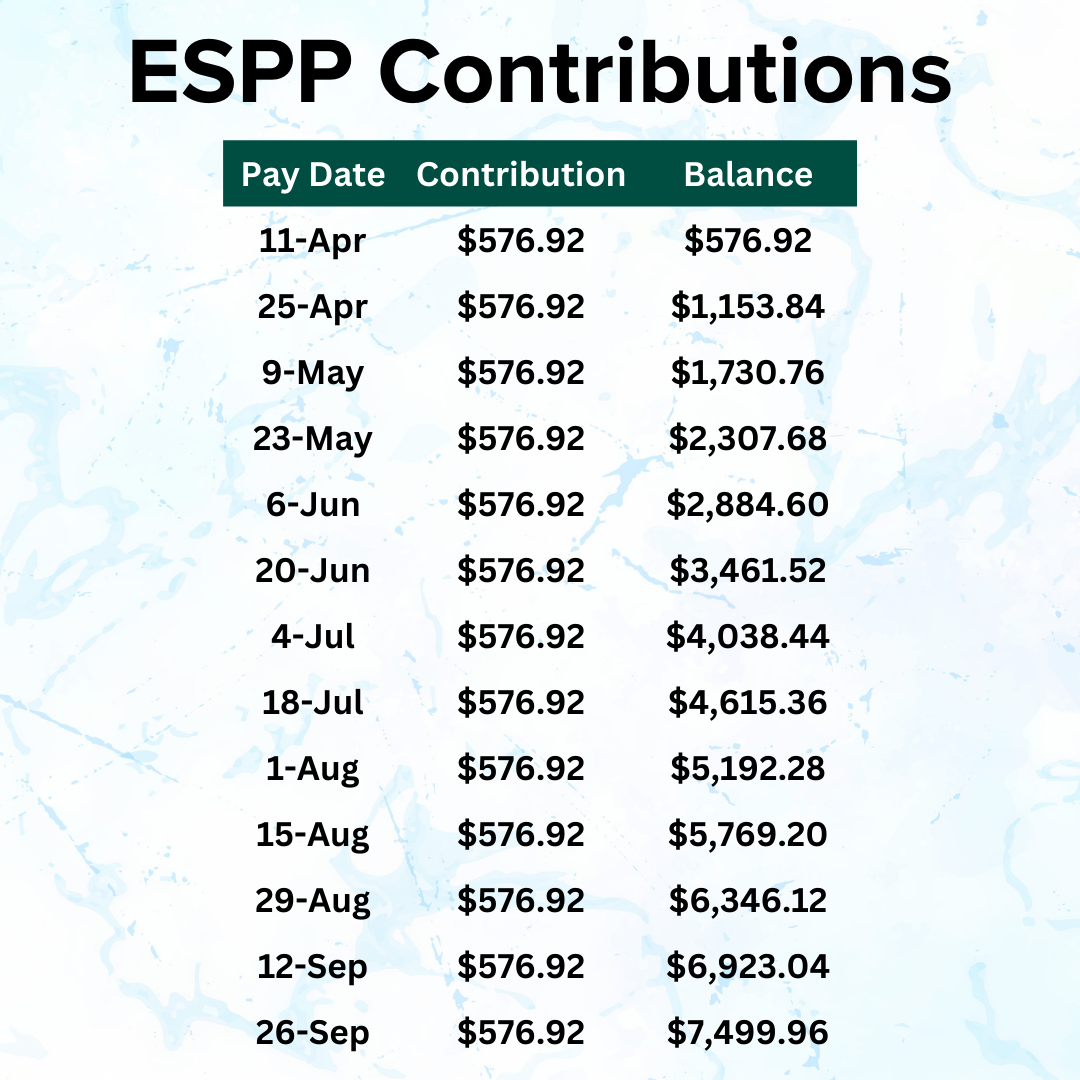

Payroll Contributions

Starting in early April, his ESPP account received $576.92 each payday ($3,846.15 * 15%). His checking account received $576.92 less with each paycheck.

Jon’s ESPP account had:

$576.92 after the first April paycheck

$1,153.84 after the second April paycheck

$1,730.76 after the first May paycheck…

After his last September paycheck, his ESPP account had a balance of $7,499.96.

Purchase

On 4/1, the company stock price was $100. Fortunately, it rose during the six months to $110 by 9/30.

To determine the purchase price, the plan administrator took 15% off the lower of the price at the beginning an end of the offering period.

That’s 15% off $100 - or $85.

Since Jon’ ESPP had $7,499.96 and the purchase price was $85, he purchased 88 shares.

He paid $7,480 ($85 * 88) for the shares. The remaining $19.96 rolled over to the next ESPP offering period.

Unrealized Gain

The shares Jon purchased are now worth $9,680 (88 * $110).

That’s an immediate gain of $2,200 ($9,680 - $7,480), or 29.4%!

He might sell them right away and pay ordinary income taxes on the entire gain.

The difference between the purchase price ($85) and the stock price on the day the stock was purchased ($110) is called the bargain element. That ordinary income would be included on Jon’s W-2. However, the gain wouldn’t be taxed Social Security or Medicare.

Cancelling Contributions

If an employee needs money before the purchase date, they may be able to cancel out of the program for the offering period. It depends on the plan.

If possible, the employee would receive cash instead of stock.

The benefit is they’ll receive much-needed cash. However, the employee would miss out on buying stock at a discount.

End of Employment

If an employee leaves the company before the purchase date - either voluntarily or involuntarily - they’ll likely receive cash, not shares. That’s not all bad as they might benefit from the extra cash then!

If someone continues to receive paychecks as part of their severance package (“garden leave”), they may stay enrolled in the ESPP. Again, it depends on the company plan.

Pros and Cons

There are many benefits and drawbacks of participating in an Employee Stock Purchase plan.

Pros

Significant upside potential

Discount lowers risk… a little

No early withdrawal penalty like with retirement plans

Bargain element is additional compensation

Discount provides leverage

A form of automatic saving

May contribute up to 15% or $25,000 each year

Cons

Not a diversified investment

Adds to employer risk (income, housing, business…)

Requires sufficient cash flow to participate

Limited ability to adjust contributions

Must remain employed until purchase date

May be subject to trading restrictions

Long holding requirements for favorable tax treatment

How Are Employee Stock Purchase Plans Taxed?

Funds employees contribute are taxed as earned income before they’re contributed to the ESPP.

Ordinary Income and Capital Gain

Normally, stock held at least a year and a day after purchase would be treated as a long-term capital gain and taxed at a lower rate. There are additional requirements for the sale of shares bought with an ESPP.

To receive partial long-term capital gains treatment, shares purchased through an ESPP need to be held:

at least two years from the start of the grant (offering date) and

one year from the purchase (purchase date).

Six Month Offering Period

For an ESPP with a six month offering period, the shares would need to be held over a year and a half after purchase.

Shares sold before that date would be considered a disqualifying disposition.

Part of the gain would likely be treated as:

ordinary income reported on the employee’s W-2 and

short-term capital gain reported on the employee’s 1099-B.

Shares generally must remain in the employee’s account with the company custodian (Fidelity, Vanguard, etc.) until they’re sold. That helps the custodian, employer, and employee file tax forms correctly!

Example 1: Sell a Month After Purchase

Let’s go back to Jon’s ESPP with a:

15% discount and

six-month lookback.

The stock did well and grew:

from $100 on 4/1 - the offering date

to $110 on 9/30 - the purchase date.

Jon’s purchase price was $85 - 15% off $100.

He then sold the shares a month later (10/30) at $115.

The sale is a disqualifying disposition because it fails both the holding requirements of over:

two years after the offering date (4/1) and

one year after purchase (9/30).

The entire discount of $25 a share ($110 - $85) is treated as ordinary income. In addition, the $5 gain since purchase is taxed as a short-term capital gain.

Example 2: Sell 19 Months After Purchase

Assume Jon instead held the stock 19 months and sold it for $130.

The sale would be a qualifying disposition because it passes both holding requirements of over:

two years after offering date (4/1) and

one year after purchase date (9/30).

In this case, only $15 of the discount ($100 - $85) is treated as ordinary income. For qualifying dispositions, the bargain element is based on the stock price on the offering date.

The remaining $30 is treated as a long-term capital gain!

Which Tax Forms Apply?

Four tax forms will likely apply to an ESPP purchase and sale:

Form 3922: purchase information

Form W-2: ordinary income (bargain element)

Form 1099-B: capital gain or loss

Form 1099-DIV: dividends

Form 3922

Perhaps the most important form is Form 3922, Transfer of Stock Acquired Through An Employee Stock Purchase Plan. It’s sent early each year to employees who participate in the plan.

Because the tax code refers to a lookback like an option, the form includes:

Date option granted = offering date

Date option exercised = purchase date

Fair market value per share on grant date = stock price on offering date

Fair market value per share on exercise date = stock price on purchase date

Exercise price paid per share = purchase price

No. of shares transferred = number of shares purchased

Date of legal title transferred = purchase date

Exercise price paid per share determined as if the option was exercised on the date shown in box 1. = purchase price if it had been purchased on the offering date

It’s critical to keep this form! The information on it is used to calculate income taxes after the stock is sold.

Tax software often assumes the employee was given the shares. However, they may only have gotten a 15% discount.

Using the details on Form 3922 can avoid paying taxes twice!

Form W-2

The definition of bargain element depends on whether the sale (disposition) is qualified or disqualified.

A disqualified disposition will likely have more of the gain taxed as ordinary income instead of long-term capital gain.

The bargain element is reported as ordinary income on the employee’s W-2.

Form 1099-B

After the employee sells the stock, they’ll receive a Form 1099-B from their custodian (Fidelity, Vanguard, etc.)

Among other things, it will include the:

purchase price and purchase date as well as the

sale price and sale date.

Depending on the sale price, the form will also report a short-term or long-term capital gain or loss.

Form 1099-DIV

If the company stock receives dividends before it’s sold, the employee will also receive a Form 1099-DIV.

Whether dividends are classified as qualified or non-qualified mostly depends on how long the shares have been held. Qualified dividends are generally taxed at the lower long-term capital gain tax brackets.

I hope this helps!

If you’re interested in a review of your specific situation…

Disclaimer

In addition to the usual disclaimers, neither this post nor these images include any financial, tax, or legal advice.