How Disability Insurance Works

By Kevin Estes

Career Stage Influences Insurance Need

Those of us who work trade time for money.

We typically start out with an ability to work decades. As we age, the years we can work falls.

Ideally, we save and invest along the way. Working also qualifies us for Social Security and, less often, pensions.

The way this plays out has major implications for insurance.

Role of Insurance

Insurance is a way to protect against mostly random bad events. Rare and expensive risks are ideal for insurance:

a medical emergency,

automobile accident,

natural disaster, et cetera.

Disability Insurance Is Critical Early

Disability insurance is critical early in careers.

After all, that's when we have the most future earnings to lose!

May Pay 40-70% of Income

Insurance is intended to help replace what someone had before a loss. That's why disability insurance is usually based on a percentage of income.

60% is somewhat standard. However, it can range from 40 to 70%.

There's often a cap, which may cause higher earners to receive less than half their regular income.

Why Are Benefits Less Than 100%?

First, benefits will be tax free if the worker pays the premiums. Those in high income tax states might see similar take home payments.

Second, the insurance companies and employers, who often pay for disability insurance, have an incentive for workers to return to work. Someone may be less dedicated to rehabilitation if they're paid as much on disability as they are working.

Third, employees are hopefully saving at least some of their income. Partial disability income replacement is yet another reason to keep expenses well below income.

Short-Term Disability

Short-term benefits typically last three to six months. After that, the worker may qualify for long-term disability benefits.

Short-term disability is usually for the worker's own occupation - or own occ. They typically receive benefits if they're unable to perform their regular responsibilities.

Long-Term Disability

The definition of long-term disability is much more variable and crucial. Many plans only offer any occupation - or any occ - coverage.

That means someone may receive little or no long-term benefits if they're able to work at all.

Importance of Own Occupation

Think of a surgeon who can no longer perform surgeries, yet can greet retail customers. For the surgeon to receive benefits based on their medical training and skills, they would have needed an own occupation - or own occ - disability policy.

There are different types of own occupation disability insurance such as modified own occupation beyond the scope of this article.

Doesn’t Social Security Pay Disability Benefits?

It does, to some extent.

However, the Social Security definition of disability is extremely limited. It generally requires someone be unable to work in any capacity.

Beware that private disability insurance benefits are often reduced by any Social Security disability benefits received.

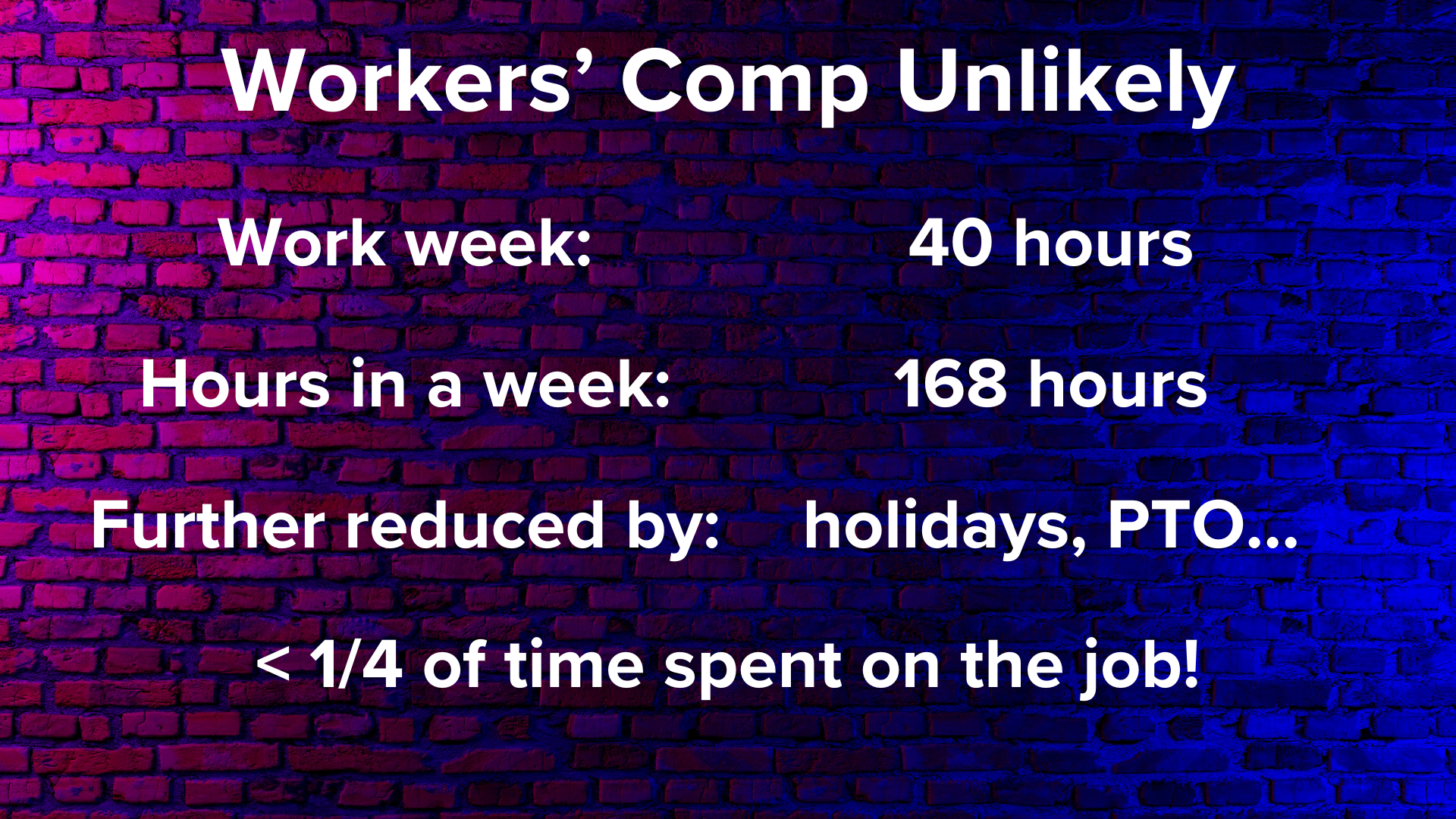

What About Workers’ Comp?

For workers compensation to apply, the cause of the disability must generally be work related and occur on the job.

The standard work week is 40 hours.

There are 168 hours in a week.

Holidays and vacations further reduce the number of hours at work.

Full time employees typically spend less than a quarter of their time on the job.

According to the Social Security Administration, only 36% of workplace disability occurs because of an accident, injury, or illness at work.

Even More Important for Families

While disability insurance is important for individuals, it's crucial for families.

With disability:

costs - especially medical - often rise

while income falls.

Employees may need disability insurance beyond an employer group plan.

Individual Policy May Be Ideal If Leaving

Individual disability may be especially important for those who plan to leave their employer. Employer disability insurance usually ends when someone leaves the company.

As an extreme example, someone who works a desk job and yearns to guide whitewater rafting trips full-time might be ahead to purchase individual disability insurance.

Rates and coverage may be much better with the desk job!

Virtuous Cycle

Fortunately, there's a bright side! Those who've saved and invested for years may already have many of their financial needs met.

All else equal, a higher net worth tends to decrease disability insurance needs. It may make sense to lower disability insurance as assets grow.

The same might be true for life insurance. Falling insurance costs are one of the many virtuous cycles with rising wealth.

If you’d like to see whether your disability insurance is adequate…

Disclaimer

In addition to the usual disclaimers, neither this post nor this video includes any financial, tax, or legal advice.